SLIDE 1

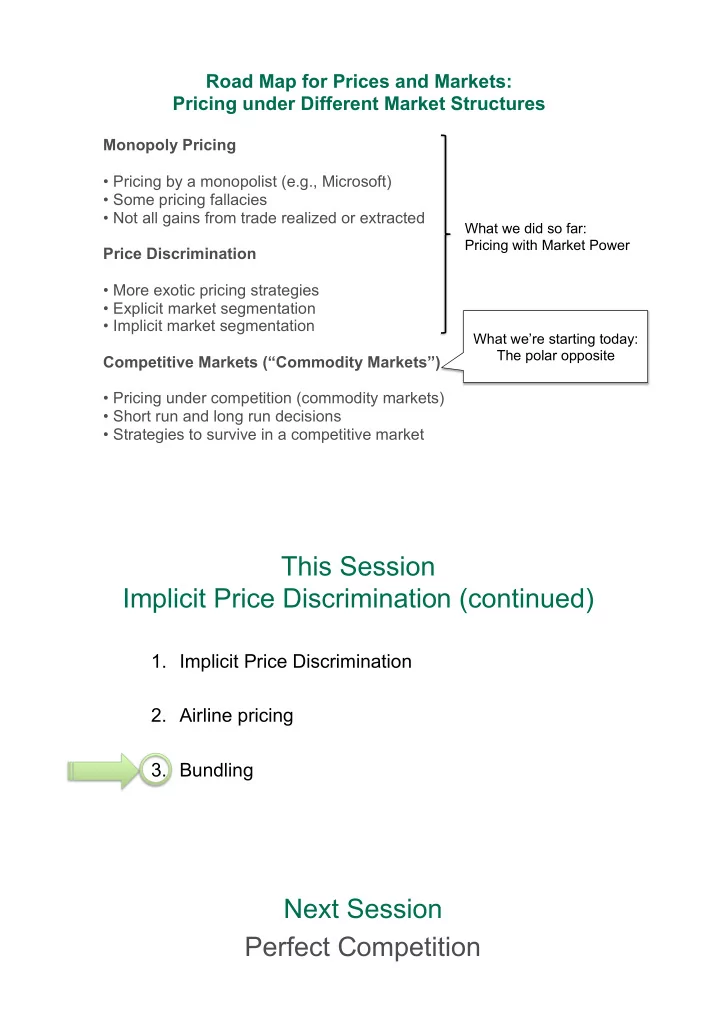

Monopoly Pricing

- Pricing by a monopolist (e.g., Microsoft)

- Some pricing fallacies

- Not all gains from trade realized or extracted

Price Discrimination

- More exotic pricing strategies

- Explicit market segmentation

- Implicit market segmentation

Competitive Markets (“Commodity Markets”)

- Pricing under competition (commodity markets)

- Short run and long run decisions

- Strategies to survive in a competitive market

Road Map for Prices and Markets: Pricing under Different Market Structures

What we’re starting today: The polar opposite What we did so far: Pricing with Market Power

This Session Implicit Price Discrimination (continued)

- 1. Implicit Price Discrimination

- 2. Airline pricing

- 3. Bundling