SLIDE 1

1

The future of (ultra) broadband in emerging markets: the Latin American case markets: the Latin American case

State of Telecom Conference

- Dr. Raúl L. Katz, Adjunct Professor, Division of

Finance and Economics, and Director, Business Strategy Research, Columbia Institute of Tele- information

Columbia Institute for Tele-Information New York, New York October 15,2011

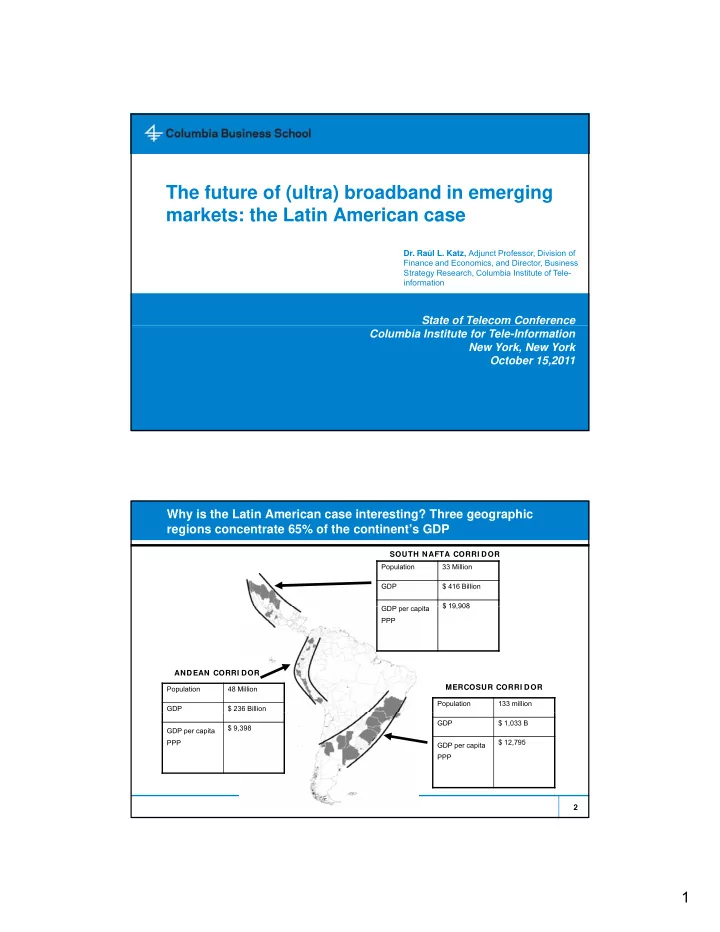

Why is the Latin American case interesting? Three geographic regions concentrate 65% of the continent’s GDP

Population 33 Million GDP $ 416 Billion GDP it $ 19 908 SOUTH NAFTA CORRI DOR Population 133 million MERCOSUR CORRI DOR GDP per capita PPP $ 19,908 Population 48 Million GDP $ 236 Billion ANDEAN CORRI DOR 2 GDP $ 1,033 B GDP per capita PPP $ 12,795 GDP per capita PPP $ 9,398