SLIDE 1

Some Special Cases

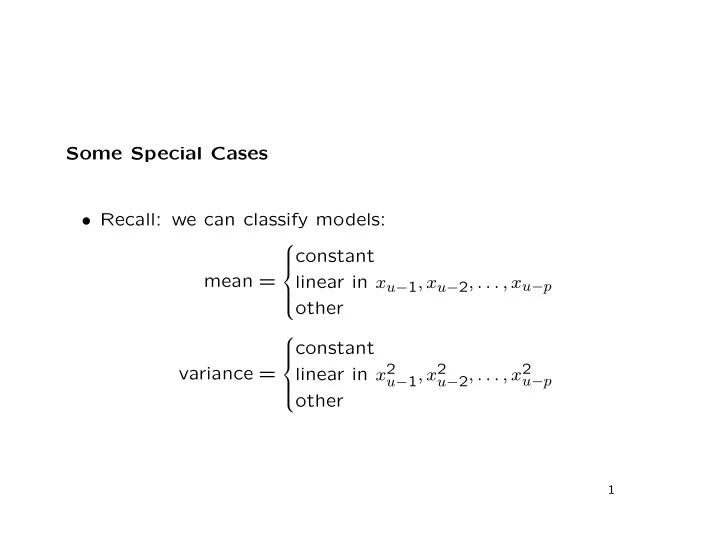

- Recall: we can classify models:

mean =

constant linear in xu−1, xu−2, . . . , xu−p

- ther

variance =

constant linear in x2

u−1, x2 u−2, . . . , x2 u−p

- ther