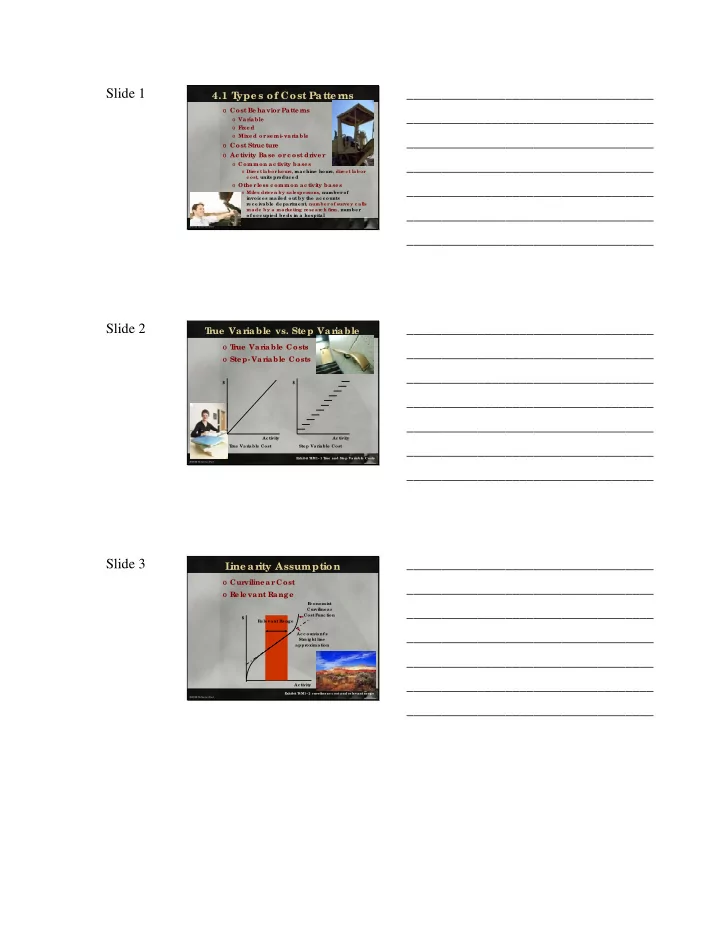

SLIDE 1

Slide 1

4.1 T ype s of Cost Patte rns

- Cost Be havior Patte r

ns

- Va ria ble

- F

ixe d

- Mixe d or se mi- varia ble

- Cost Str

uc tur e

- Ac tivity Ba se or c ost dr

ive r

- Common a c tivity ba se s

- Dire c t labor hours, ma c hine hours, dire c t la bor

c ost, units produc e d

- Othe r

le ss c ommon ac tivity ba se s

- Mile s drive n by sale spe rsons, number of

invoic e s ma iled out by the ac c ounts rec e iva ble de pa rtme nt, numbe r of surve y c a lls made by a marketing re se a rc h firm, number

- f oc c upie d be ds in a hospita l

2005 K D Ha the wa y-Dia l

___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ Slide 2

T r ue Var iable vs. Ste p Var iable

- T

rue Variable Costs

- Ste p- Va r

iable Costs

Ste p Va r ia ble Cost $ $ Ac tivity

E xhibit T 4M1~1 T rue and Ste p Variable Costs

Ac tivity T r ue Va r ia ble Cost

2005 K D Ha the wa y-Dia l

___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ ___________________________________ Slide 3

L ine arity Assumption

- Curviline a r Cost

- Re le vant Rang e

R e le va nt Ra ng e Ac c ounta nt’s Stra ig ht line a pproxima tion E c onomist Curviline a r Cost F unc tion $ Ac tivity

Exhibit T 4M1~2 c urviline a r c ost a nd re le vant rang e

2005 K D Ha the wa y-Dia l