SLIDE 1

1

L&S Offices: New Delhi | Gurugram | Mumbai | Kolkata | Chennai | Cochin | Jaipur Bengaluru | Hyderabad | Allahabad | Ahmedabad | Chandigarh | Pune An ISO 9001:2008 and ISO 27001:2013 certified law firm

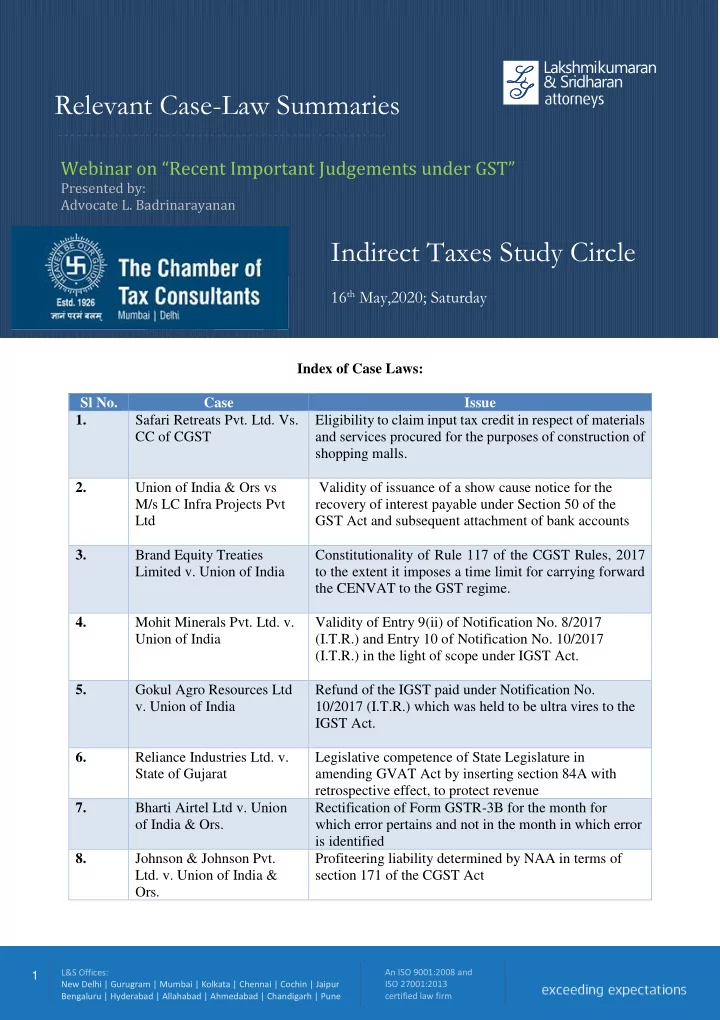

Index of Case Laws: Sl No. Case Issue 1. Safari Retreats Pvt. Ltd. Vs. CC of CGST Eligibility to claim input tax credit in respect of materials and services procured for the purposes of construction of shopping malls. 2. Union of India & Ors vs M/s LC Infra Projects Pvt Ltd Validity of issuance of a show cause notice for the recovery of interest payable under Section 50 of the GST Act and subsequent attachment of bank accounts 3. Brand Equity Treaties Limited v. Union of India Constitutionality of Rule 117 of the CGST Rules, 2017 to the extent it imposes a time limit for carrying forward the CENVAT to the GST regime. 4. Mohit Minerals Pvt. Ltd. v. Union of India Validity of Entry 9(ii) of Notification No. 8/2017 (I.T.R.) and Entry 10 of Notification No. 10/2017 (I.T.R.) in the light of scope under IGST Act. 5. Gokul Agro Resources Ltd

- v. Union of India

Refund of the IGST paid under Notification No. 10/2017 (I.T.R.) which was held to be ultra vires to the IGST Act. 6. Reliance Industries Ltd. v. State of Gujarat Legislative competence of State Legislature in amending GVAT Act by inserting section 84A with retrospective effect, to protect revenue 7. Bharti Airtel Ltd v. Union

- f India & Ors.

Rectification of Form GSTR-3B for the month for which error pertains and not in the month in which error is identified 8. Johnson & Johnson Pvt.

- Ltd. v. Union of India &