SLIDE 1

1

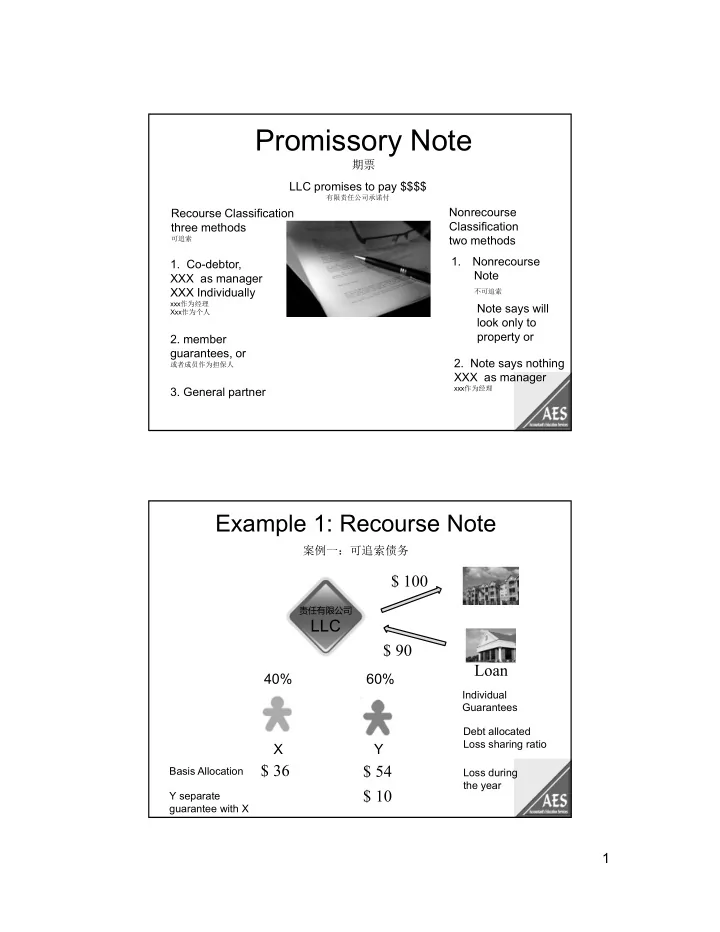

Promissory Note

期票 LLC promises to pay $$$$

有限责任公司承诺付

- 1. Co-debtor,

XXX as manager XXX Individually

xxx作为经理 Xxx作为个人

Recourse Classification three methods

可追索

Note says will look only to property or

- 2. Note says nothing

XXX as manager

xxx作为经理

- 2. member

guarantees, or

或者成员作为担保人

Nonrecourse Classification two methods

- 3. General partner

1. Nonrecourse Note

不可追索

Example 1: Recourse Note

案例一:可追索债务

责任有限公司

LLC

40% X 60% Y

Basis Allocation

$ 36 $ 54 $ 90 Loan $ 100

Loss during the year Individual Guarantees Debt allocated Loss sharing ratio Y separate guarantee with X