SLIDE 5 5

9

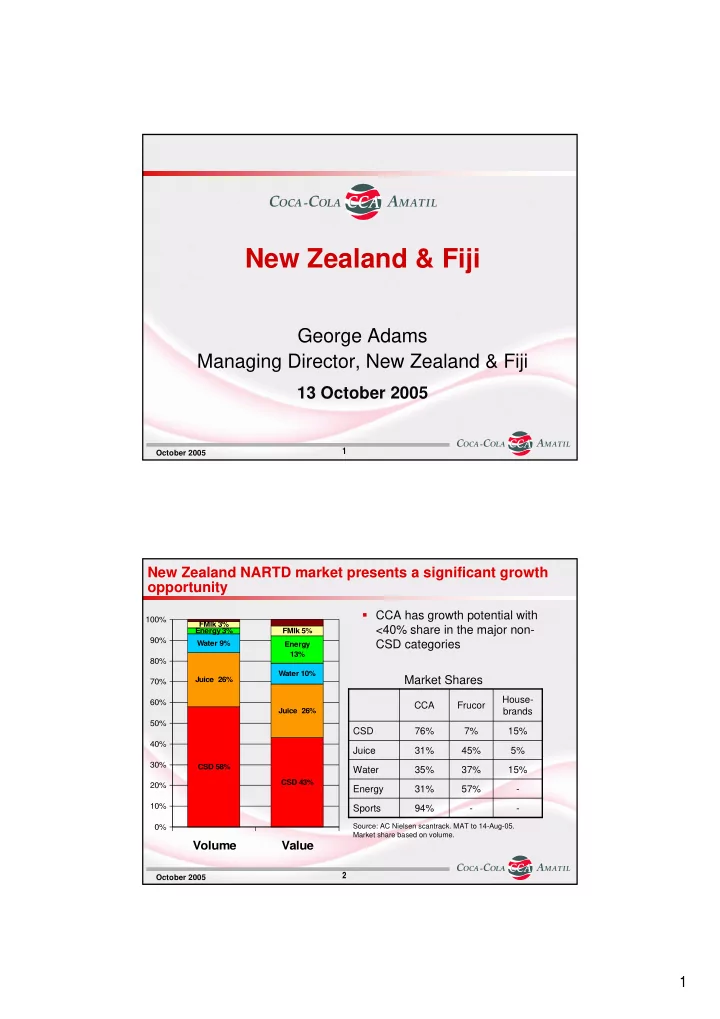

October 2005

World First – Coke Raspberry

In a global first for the Coca-Cola System, New Zealand launched ‘Coke with Raspberry’ and ‘diet Coke with Raspberry’ in June 2005 It was the first time that the Coca-Cola flavour and the diet Coke flavour have been launched simultaneously Sales are in line with expectations Early 2006 rotation planned

10

October 2005

20.7% 20.5% 20.0% 19.8% 19.5% 19.4% 19.0% 19.2% 19.2% 19.3% 19.4% 19.6% 19.8% 20.3% 12.5% 12.6% 12.7% 12.5% 12.6% 12.4% 12.6% 12.6% 12.8% 13.0% 12.9% 13.2% 13.4% 13.6% 4.6% 4.7% 5.0% 5.2% 5.7% 6.1% 6.4% 6.7% 6.9% 7.0% 7.1% 7.2% 7.5% 7.6% 1.9% 1.9% 1.9% 1.9% 2.0% 2.1% 2.2% 2.2% 2.3% 2.4% 2.4% 2.2% 2.1% 2.1% 20.1% 20.7% 21.1% 21.6% 21.8% 22.3% 22.7% 23.1% 23.3% 23.3% 23.5% 23.3% 23.0% 22.5% 7.5% 7.4% 7.5% 7.5% 7.5% 7.5% 7.3% 7.2% 7.1% 7.1% 7.1% 7.1% 7.0% 6.9% 3.0% 2.9% 2.6% 2.5% 2.2% 1.9% 1.7% 1.6% 1.4% 1.3% 1.1% 0.9% 0.8% 0.7% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.2% 3.3% 3.4% 3.4% 3.5% 3.6% 3.6% 3.7% 3.8% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.7% 3.6% 4.6% 4.4% 4.3% 4.2% 4.1% 3.9% 3.8% 3.7% 3.7% 3.6% 3.6% 3.5% 3.4% 3.4% 8.3% 8.0% 7.8% 7.7% 7.4% 7.1% 6.8% 6.4% 5.8% 5.5% 5.2% 5.0% 5.0% 4.9% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 12 SEP 04 10 OCT 04 07 NOV 04 05 DEC 04 02 JAN 05 30 JAN 05 27 FEB 05 27 MAR 05 24 APR 05 22 MAY 05 19 JUN 05 17 JUL 05 14 AUG 05 11 SEP 05

- T. JUST JUICE

- T. FRESH UP

- T. CITRUS TREE

- T. TWIST

- T. KERI

- T. KERI THEXTONS

- T. KERI SPLICE

- T. SIMPLY SQUEEZED

- T. CHARLIES

- T. GOLDEN CIRCLE

TOTAL CONTROLLED LABEL

MAT Fruit Juice/Drinks Brand Shares | Grocery

Maintained excellent juice market share over past 12 months despite heavy competition

Keri Brand #1