SLIDE 1

1

Investor Tour – New Zealand

New Zealand A robust business model

George Adams 16-17 October 2008

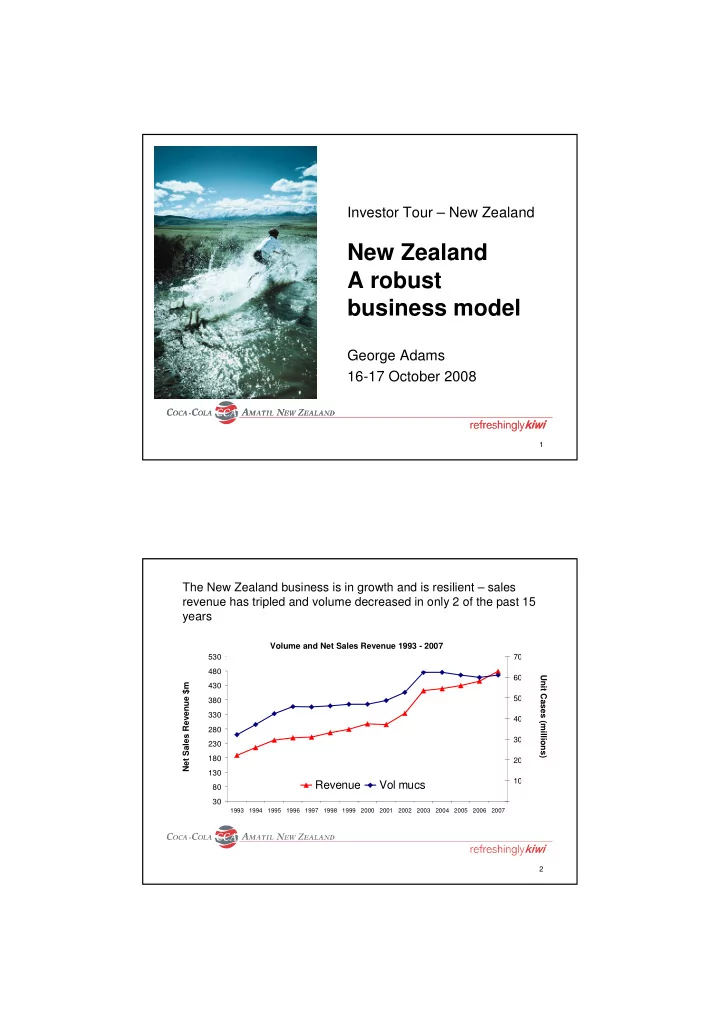

2 30 80 130 180 230 280 330 380 430 480 530

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Net Sales Revenue (NZD $m) 10 20 30 40 50 60 70 Unit Cases (millions)

Revenue Vol mucs The New Zealand business is in growth and is resilient – sales revenue has tripled and volume decreased in only 2 of the past 15 years

Volume and Net Sales Revenue 1993 - 2007 Net Sales Revenue $m Unit Cases (millions)