June 1, 2007

New Challenge 10 New Challenge 10

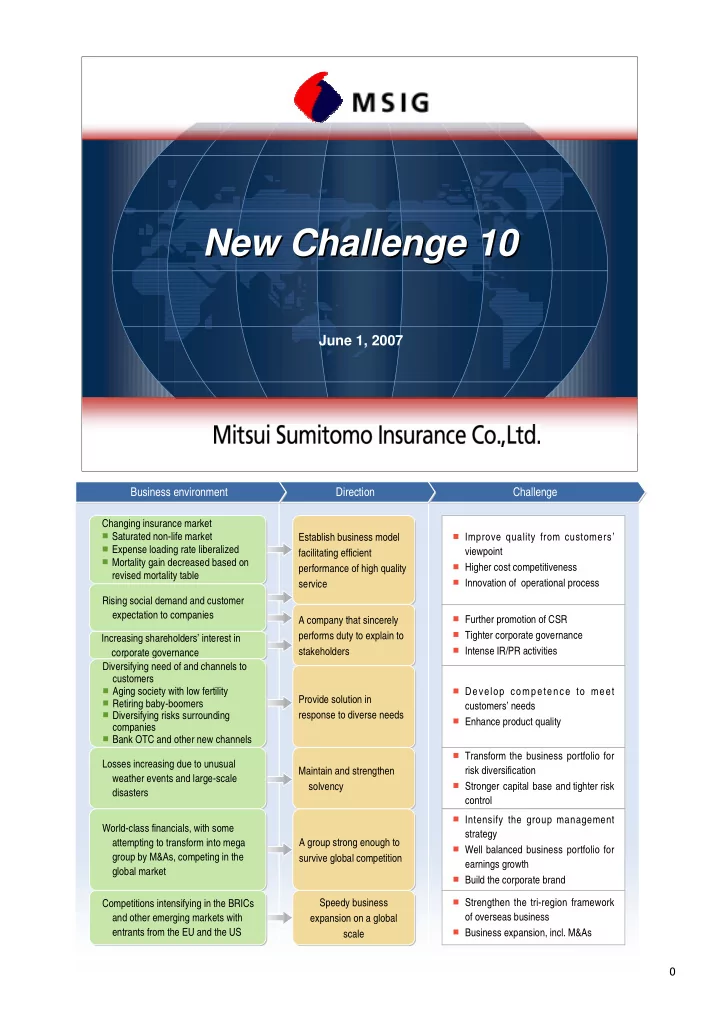

Improve quality from customers’

viewpoint

Higher cost competitiveness Innovation of operational process

Establish business model facilitating efficient performance of high quality service Establish business model facilitating efficient performance of high quality service A company that sincerely performs duty to explain to stakeholders A company that sincerely performs duty to explain to stakeholders Provide solution in response to diverse needs Provide solution in response to diverse needs Maintain and strengthen solvency Maintain and strengthen solvency A group strong enough to survive global competition A group strong enough to survive global competition Speedy business expansion on a global scale Speedy business expansion on a global scale

Further promotion of CSR Tighter corporate governance Intense IR/PR activities Develop competence to meet

customers’ needs

Enhance product quality Transform the business portfolio for

risk diversification

Stronger capital base and tighter risk

control

Intensify the group management

strategy

Well balanced business portfolio for

earnings growth

Build the corporate brand Strengthen the tri-region framework

- f overseas business

Business expansion, incl. M&As

Challenge Challenge Direction Direction Business environment Business environment

Changing insurance market

Saturated non-life market Expense loading rate liberalized Mortality gain decreased based on

revised mortality table Changing insurance market

Saturated non-life market Expense loading rate liberalized Mortality gain decreased based on

revised mortality table Rising social demand and customer expectation to companies Rising social demand and customer expectation to companies Increasing shareholders’ interest in corporate governance Increasing shareholders’ interest in corporate governance Diversifying need of and channels to customers

Aging society with low fertility Retiring baby-boomers Diversifying risks surrounding

companies

Bank OTC and other new channels

Diversifying need of and channels to customers

Aging society with low fertility Retiring baby-boomers Diversifying risks surrounding

companies

Bank OTC and other new channels

Losses increasing due to unusual weather events and large-scale disasters Losses increasing due to unusual weather events and large-scale disasters World-class financials, with some attempting to transform into mega group by M&As, competing in the global market World-class financials, with some attempting to transform into mega group by M&As, competing in the global market Competitions intensifying in the BRICs and other emerging markets with entrants from the EU and the US Competitions intensifying in the BRICs and other emerging markets with entrants from the EU and the US