SLIDE 1

Managing Security Investment

Part III Tyler Moore

Computer Science & Engineering Department, SMU, Dallas, TX

September 25, 2012

Gordon-Loeb model Baseline models

Outline

1

Gordon-Loeb model Breach probability function Decreasing marginal returns Optimal security investment

2

Baseline models Linear breach probability function Exponential breach probability function Investment models in R

2 / 31 Gordon-Loeb model Baseline models

Review of security investment so far

Metrics for quantifying security benefits

1

ALE0: expected loss without security investment

2

ALEs: expected loss with security investment

3

EBISs: ALE0 − ALEs

4

ENBISs: ALE0 − ALEs − c

High-level investment metrics

1

ROSI

2

NPV

3

IRR

3 / 31 Gordon-Loeb model Baseline models

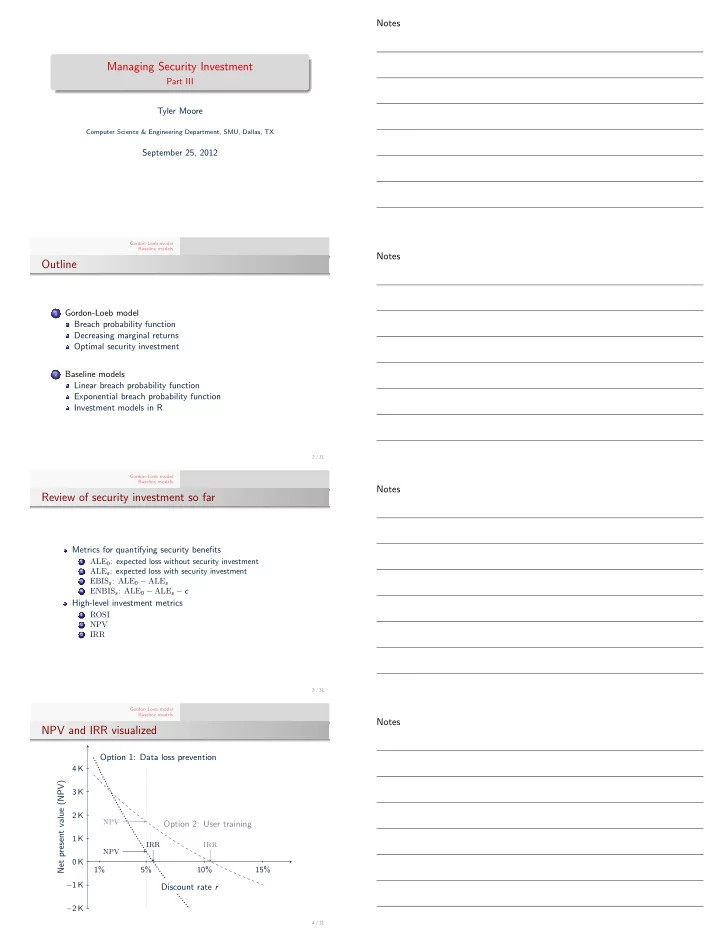

NPV and IRR visualized

Net present value (NPV)

−2 K −1 K 0 K 1 K 2 K 3 K 4 K

Discount rate r

1% 5% 10% 15%

Option 1: Data loss prevention Option 2: User training

NPV NPV IRR IRR

4 / 31