SLIDE 1

M O N E Y M A N A G E M E N T I N S T I T U T E

1737 H Street NW, 5

th Floor, Washington, DC 20006 • Phone: (202) 822-4949 • Fax: (202) 822-5188 • www.MMInst.org

Key Findings from the Money Management Institute’s 2016 Edition of Distribution of Alternative Investments through Wirehouses

After Years of Steady Growth, Alternative Investment Assets at Wirehouses Fall 4% in 2016 with All of the Decline Attributable to Liquid Alternatives

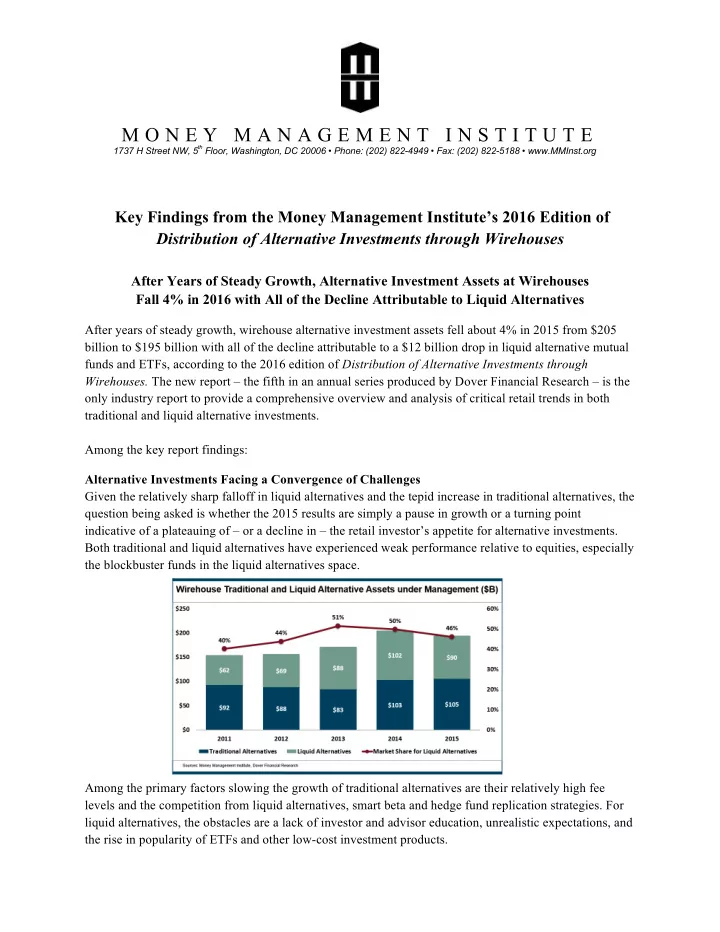

After years of steady growth, wirehouse alternative investment assets fell about 4% in 2015 from $205 billion to $195 billion with all of the decline attributable to a $12 billion drop in liquid alternative mutual funds and ETFs, according to the 2016 edition of Distribution of Alternative Investments through

- Wirehouses. The new report – the fifth in an annual series produced by Dover Financial Research – is the

- nly industry report to provide a comprehensive overview and analysis of critical retail trends in both