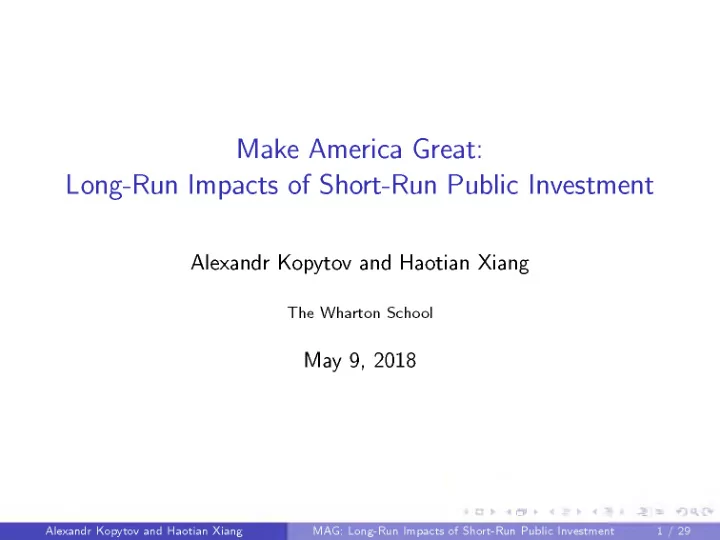

SLIDE 2 £ + F o llo w D o n a ld J . T ru m p O @realDonaldTrump

T h e ro a d s a n d s id e w a lk s , a irp o rts a n d b rid g e s , a re p e rfe c t in D u b a i. E v e ry th in g lo o k s c le a n & s tro n g . In U .S ., e v e ry th in g is fa llin g a p a rt!

RETWEETS LIKES 71 ־ g£Q-.

I *

257 258 i i B £. X A

¥ \\ 3 1

7:33 AM -1 9 May 2014 134 257 V 258

E

H illa ry C lin to n O 3

±* F o llo w

v @HillaryClinton

In v e s tin g in o u r in fra s tru c tu re is a b o u t m o re th a n c re a tin g g o o d jo b s : it's a b o u t m a in ta in in g o u r s ta tu s a s th e w o r ld ’s e c o n o m ic s u p e rp o w e r.

RETWEETS LIKES r 4 ־ k. t v ~ ■OB ■ ■ i

598 1,335

7:06 PM -3 0 Nov 2015

♦ » 184 598 V 1.3K

< □ ►

4 i f ► 4 0 ^ 0־ =51■ ► 5 » ► ן

M A G : L o n g - R u n Im p a c ts o f S h o r t - R u n P u b lic I n v e s tm e n t 2 / 2 9 A le x a n d r K o p y t o v a n d H a o tia n X ia n g