SLIDE 1

1

Lecture 3.1: Option Pricing Models: The Binomial Model

Nattawut Jenwittayaroje, PhD, CFA

NIDA Business School

National Institute of Development Administration

01135534: Financial Modelling

2

Important Concepts

The concept of an option pricing model The one‐ and two‐period binomial option pricing models Explanation of the establishment and maintenance of a risk‐free hedge Illustration of how early exercise can be captured The extension of the binomial model to any number of time periods

3

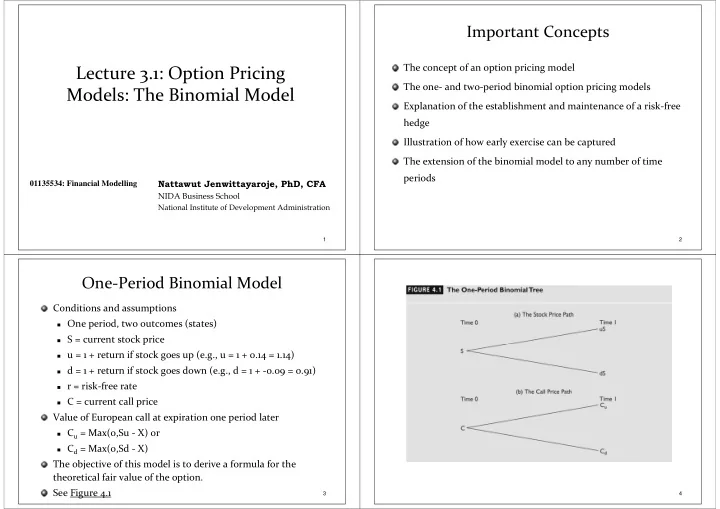

One‐Period Binomial Model

Conditions and assumptions

One period, two outcomes (states) S = current stock price u = 1 + return if stock goes up (e.g., u = 1 + 0.14 = 1.14) d = 1 + return if stock goes down (e.g., d = 1 + ‐0.09 = 0.91) r = risk‐free rate C = current call price

Value of European call at expiration one period later

Cu = Max(0,Su ‐ X) or Cd = Max(0,Sd ‐ X)

The objective of this model is to derive a formula for the theoretical fair value of the option. See Figure 4.1

4