SLIDE 1

KEY INDIVIDUAL PROVISIONS

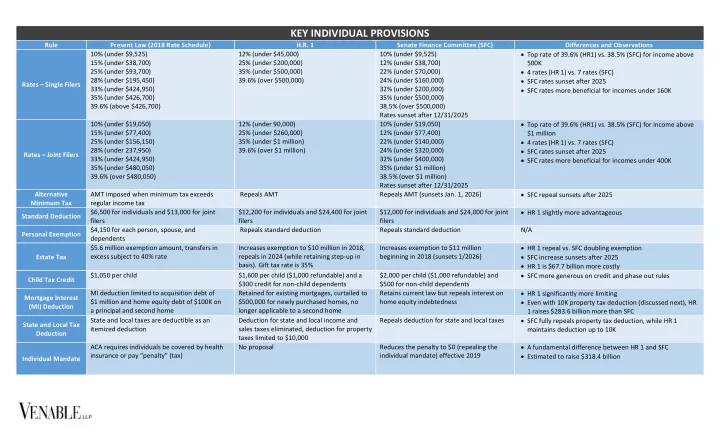

Rule Present Law (2018 Rate Schedule) H.R. 1 Senate Finance Committee (SFC) Differences and Observations Rates – Single Filers 10% (under $9,525) 15% (under $38,700) 25% (under $93,700) 28% (under $195,450) 33% (under $424,950) 35% (under $426,700) 39.6% (above $426,700) 12% (under $45,000) 25% (under $200,000) 35% (under $500,000) 39.6% (over $500,000) 10% (under $9,525) 12% (under $38,700) 22% (under $70,000) 24% (under $160,000) 32% (under $200,000) 35% (under $500,000) 38.5% (over $500,000) Rates sunset after 12/31/2025 Top rate of 39.6% (HR1) vs. 38.5% (SFC) for income above 500K 4 rates (HR 1) vs. 7 rates (SFC) SFC rates sunset after 2025 SFC rates more beneficial for incomes under 160K Rates – Joint Filers 10% (under $19,050) 15% (under $77,400) 25% (under $156,150) 28% (under 237,950) 33% (under $424,950) 35% (under $480,050) 39.6% (over $480,050) 12% (under 90,000) 25% (under $260,000) 35% (under $1 million) 39.6% (over $1 million) 10% (under $19,050) 12% (under $77,400) 22% (under $140,000) 24% (under $320,000) 32% (under $400,000) 35% (under $1 million) 38.5% (over $1 million) Rates sunset after 12/31/2025 Top rate of 39.6% (HR1) vs. 38.5% (SFC) for income above $1 million 4 rates (HR 1) vs. 7 rates (SFC) SFC rates sunset after 2025 SFC rates more beneficial for incomes under 400K Alternative Minimum Tax AMT imposed when minimum tax exceeds regular income tax Repeals AMT Repeals AMT (sunsets Jan. 1, 2026) SFC repeal sunsets after 2025 Standard Deduction $6,500 for individuals and $13,000 for joint filers $12,200 for individuals and $24,400 for joint filers $12,000 for individuals and $24,000 for joint filers HR 1 slightly more advantageous Personal Exemption $4,150 for each person, spouse, and dependents Repeals standard deduction Repeals standard deduction N/A Estate Tax $5.6 million exemption amount, transfers in excess subject to 40% rate Increases exemption to $10 million in 2018, repeals in 2024 (while retaining step-up in basis). Gift tax rate is 35% Increases exemption to $11 million beginning in 2018 (sunsets 1/2026) HR 1 repeal vs. SFC doubling exemption SFC increase sunsets after 2025 HR 1 is $67.7 billion more costly Child Tax Credit $1,050 per child $1,600 per child ($1,000 refundable) and a $300 credit for non-child dependents $2,000 per child ($1,000 refundable) and $500 for non-child dependents SFC more generous on credit and phase out rules Mortgage Interest (MI) Deduction MI deduction limited to acquisition debt of $1 million and home equity debt of $100K on a principal and second home Retained for existing mortgages, curtailed to $500,000 for newly purchased homes, no longer applicable to a second home Retains current law but repeals interest on home equity indebtedness HR 1 significantly more limiting Even with 10K property tax deduction (discussed next), HR 1 raises $283.6 billion more than SFC State and Local Tax Deduction State and local taxes are deductible as an itemized deduction Deduction for state and local income and sales taxes eliminated, deduction for property taxes limited to $10,000 Repeals deduction for state and local taxes SFC fully repeals property tax deduction, while HR 1 maintains deduction up to 10K Individual Mandate ACA requires individuals be covered by health insurance or pay “penalty” (tax) No proposal Reduces the penalty to $0 (repealing the individual mandate) effective 2019 A fundamental difference between HR 1 and SFC Estimated to raise $318.4 billion