SLIDE 1

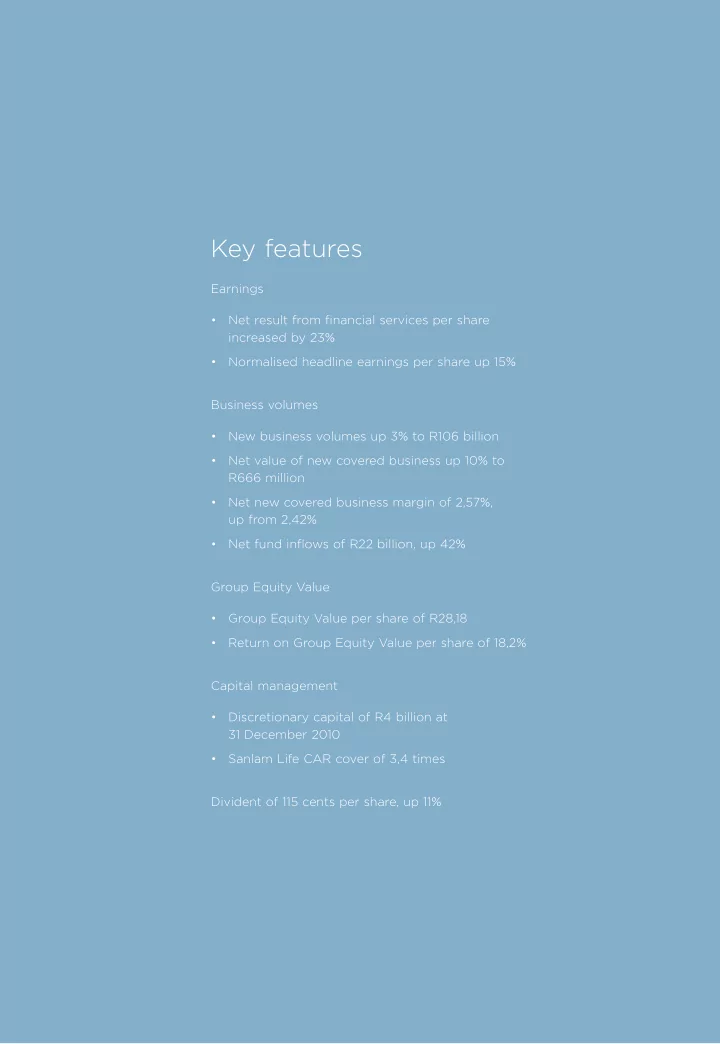

Key features

Earnings

- Net result from fjnancial services per share

increased by 23%

- Normalised headline earnings per share up 15%

Business volumes

- New business volumes up 3% to R106 billion

- Net value of new covered business up 10% to

R666 million

- Net new covered business margin of 2,57%,

up from 2,42%

- Net fund infmows of R22 billion, up 42%

Group Equity Value

- Group Equity Value per share of R28,18

- Return on Group Equity Value per share of 18,2%

Capital management

- Discretionary capital of R4 billion at

31 December 2010

- Sanlam Life CAR cover of 3,4 times

Divident of 115 cents per share, up 11%