SLIDE 1

ING Office Fund Acquisition of the Homer Building, Washington DC - - PowerPoint PPT Presentation

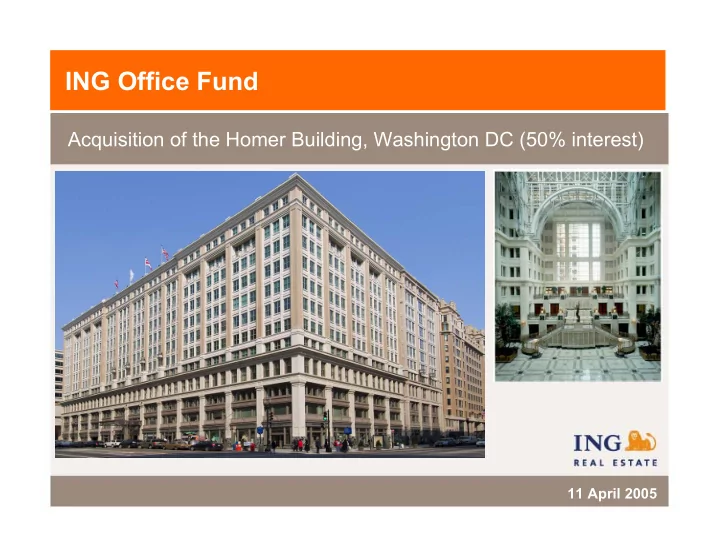

ING Office Fund Acquisition of the Homer Building, Washington DC (50% interest) 11 April 2005 Transaction summary Key benefits One of Washington DCs most prominent and finest office buildings Outstanding location - 3 blocks from the

* Guaranteed minimum NOI yield of 6.5% for years 1 - 3

Skylight twelve-storey atrium Tenancy foyer

Dallas New York Washington DC

Existing IOF Assets Homer Building

Homer Building

White House

Source: Torto Wheaton, Economy.com, ING Real Estate

* AUD/USD spot = 0.765

QLD 13% NSW 45% ACT 5% WA 2% NY 8% Washington DC 7% Dallas 4% VIC 16% QLD 12% NSW 41% ACT 5% WA 2% NY 8% Washington DC 13% Dallas 4% VIC 15%

** DRP to be introduced from Jun-05 quarter * USD/AUD spot = 0.765

* USD/AUD spot = 0.765 Indicative rates only. Include margins.