CRISIL Equities

Zylog Systems Limited

1

Independent Research Report – Zylog Systems Limited Independent Research Report – Zylog Systems Limited

Chasing diversified growth opportunities

Industry: Information Technology Date: May 7, 2010 Zylog Systems Ltd (Zylog), headquartered in Chennai, is a niche IT services player with a focus on products, solutions and mobile technologies. We assign Zylog a fundamental grade

- f ‘3/5’ indicating that its fundamentals are ‘Good’ relative to other listed securities in India.

We also assign a valuation grade of ‘4/5’ indicating an ‘Upside’ to the current market price. Chasing diversified growth opportunities Zylog is currently pursuing various new initiatives for growth in the IT services and telecom

- space. These include: (a) the recent acquisition of Brainhunter, one of the leading Canadian

staffing companies; (b) various e-governance projects in the transportation, healthcare, agriculture sectors, and related to below poverty line population; (c) Wi-Fi-based internet service offerings in the tier-I and tier-II cities in southern India, where it has a deep-rooted

- presence. We believe that these initiatives position Zylog well for strong growth. We expect

Wi-Fi revenues to grow to Rs 1.2 bn by FY15 and e-governance revenues to touch Rs 0.8 bn, a 9% revenue contribution from zero contribution currently. Inorganic growth strategy has strengthened its offering and client base Zylog, a niche IT services player, has strengthened its offerings and reach through strategic acquisitions made over the past three years. Zylog has successfully integrated the acquired products, solutions and services into its suite of offerings. These acquisitions have helped Zylog penetrate the market deeper and cross-sell its newly-acquired offerings to complementary markets. Key challenges include integration of Brainhunter and competition in Wi-Fi (a) Brainhunter is a larger company (in revenues terms) than Zylog and is into staffing solutions, while other acquisitions were small in size and in the IT solutions space. Also, Brainhunter had filed for Companies' Creditors Arrangement Act to avoid bankruptcy. Hence, successful integration is a key monitorable. (b) In the longer term, the Wi-Fi business is expected to face significant competition from the telecom majors, resulting in margin erosion. Revenues to grow at three-year CAGR of 37% due to Brainhunter acquisition We expect consolidated revenues to grow 37% over FY10-13 to Rs 23 bn on account of the Brainhunter acquisition, while the standalone revenues are set to register a CAGR of 22% in rupee terms. However, EBITDA margins are estimated to decline to 11% in FY13 on account

- f (a) 400 bps impact of Brainhunter acquisition; (b) 300 bps reduction in offshore utilisation

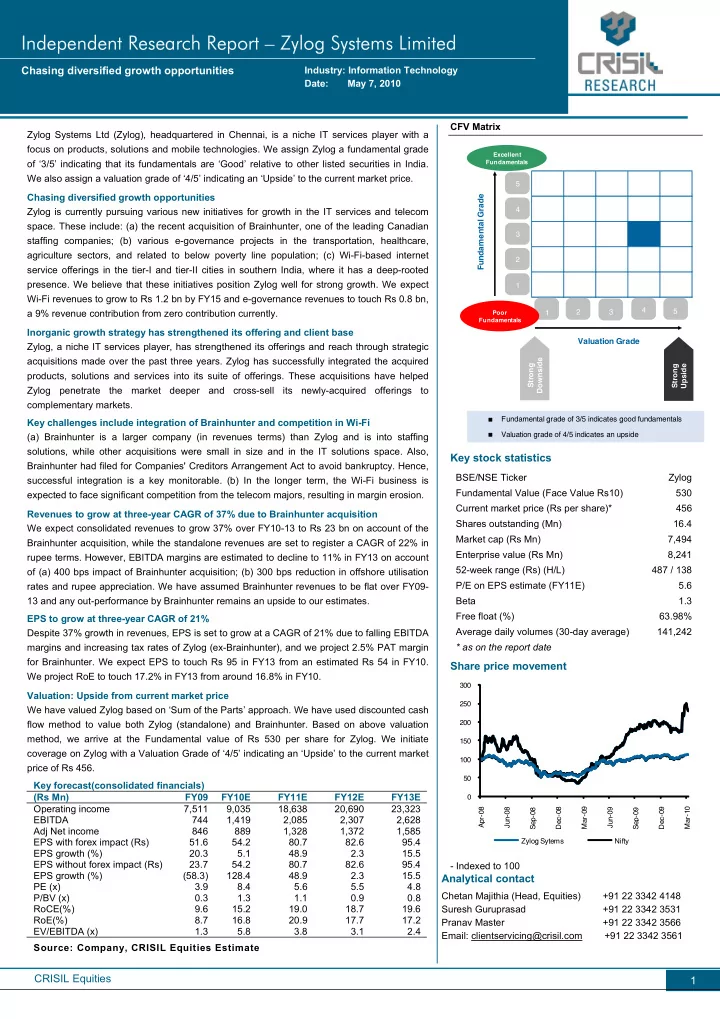

rates and rupee appreciation. We have assumed Brainhunter revenues to be flat over FY09- 13 and any out-performance by Brainhunter remains an upside to our estimates. EPS to grow at three-year CAGR of 21% Despite 37% growth in revenues, EPS is set to grow at a CAGR of 21% due to falling EBITDA margins and increasing tax rates of Zylog (ex-Brainhunter), and we project 2.5% PAT margin for Brainhunter. We expect EPS to touch Rs 95 in FY13 from an estimated Rs 54 in FY10. We project RoE to touch 17.2% in FY13 from around 16.8% in FY10. Valuation: Upside from current market price We have valued Zylog based on ‘Sum of the Parts’ approach. We have used discounted cash flow method to value both Zylog (standalone) and Brainhunter. Based on above valuation method, we arrive at the Fundamental value of Rs 530 per share for Zylog. We initiate coverage on Zylog with a Valuation Grade of ‘4/5’ indicating an ‘Upside’ to the current market price of Rs 456. Key forecast(consolidated financials) (Rs Mn) FY09 FY10E FY11E FY12E FY13E Operating income 7,511 9,035 18,638 20,690 23,323 EBITDA 744 1,419 2,085 2,307 2,628 Adj Net income 846 889 1,328 1,372 1,585 EPS with forex impact (Rs) 51.6 54.2 80.7 82.6 95.4 EPS growth (%) 20.3 5.1 48.9 2.3 15.5 EPS without forex impact (Rs) 23.7 54.2 80.7 82.6 95.4 EPS growth (%) (58.3) 128.4 48.9 2.3 15.5 PE (x) 3.9 8.4 5.6 5.5 4.8 P/BV (x) 0.3 1.3 1.1 0.9 0.8 RoCE(%) 9.6 15.2 19.0 18.7 19.6 RoE(%) 8.7 16.8 20.9 17.7 17.2 EV/EBITDA (x) 1.3 5.8 3.8 3.1 2.4 Source: Company, CRISIL Equities Estimate CFV Matrix

Fundamental grade of 3/5 indicates good fundamentals Valuation grade of 4/5 indicates an upside 1 2 3 4 5 1 2 3 4 5

Valuation Grade Fundamental Grade

Poor Fundamentals Excellent Fundamentals

Strong Downside Strong Upside

Key stock statistics

BSE/NSE Ticker Zylog Fundamental Value (Face Value Rs10) 530 Current market price (Rs per share)* 456 Shares outstanding (Mn) 16.4 Market cap (Rs Mn) 7,494 Enterprise value (Rs Mn) 8,241 52-week range (Rs) (H/L) 487 / 138 P/E on EPS estimate (FY11E) 5.6 Beta 1.3 Free float (%) 63.98% Average daily volumes (30-day average) 141,242 * as on the report date

Share price movement

50 100 150 200 250 300 Apr-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Zylog Sytems Nifty

- Indexed to 100

Analytical contact

Chetan Majithia (Head, Equities) +91 22 3342 4148 Suresh Guruprasad +91 22 3342 3531 Pranav Master +91 22 3342 3566 Email: clientservicing@crisil.com +91 22 3342 3561