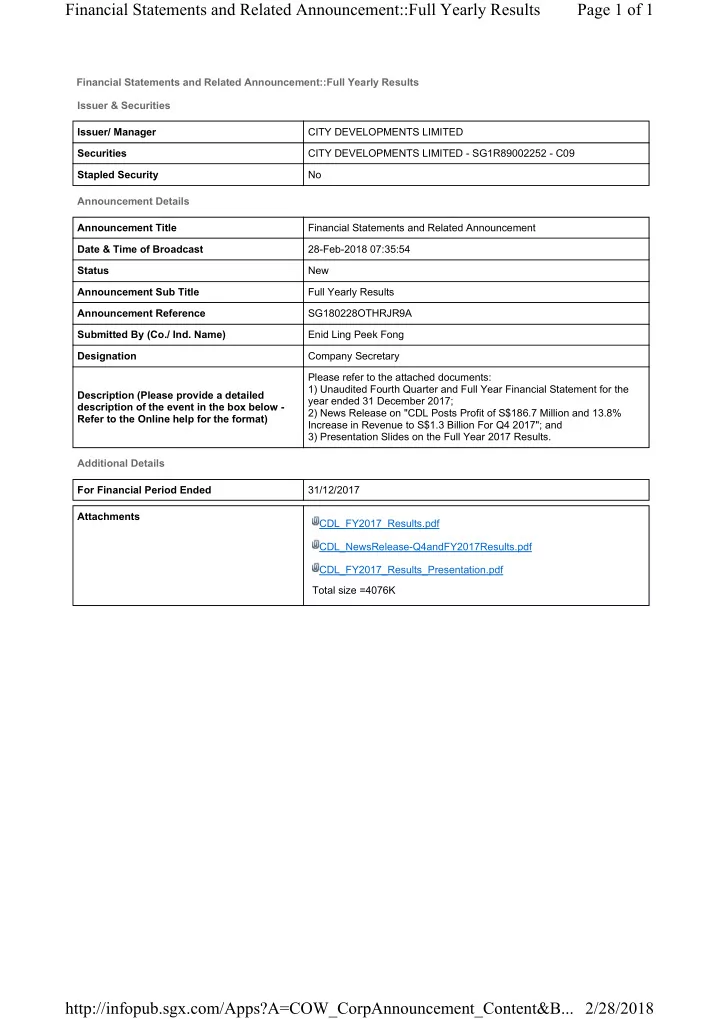

Financial Statements and Related Announcement::Full Yearly Results Issuer & Securities Issuer/ Manager CITY DEVELOPMENTS LIMITED Securities CITY DEVELOPMENTS LIMITED - SG1R89002252 - C09 Stapled Security No Announcement Details Announcement Title Financial Statements and Related Announcement Date & Time of Broadcast 28-Feb-2018 07:35:54 Status New Announcement Sub Title Full Yearly Results Announcement Reference SG180228OTHRJR9A Submitted By (Co./ Ind. Name) Enid Ling Peek Fong Designation Company Secretary Description (Please provide a detailed description of the event in the box below - Refer to the Online help for the format) Please refer to the attached documents: 1) Unaudited Fourth Quarter and Full Year Financial Statement for the year ended 31 December 2017; 2) News Release on "CDL Posts Profit of S$186.7 Million and 13.8% Increase in Revenue to S$1.3 Billion For Q4 2017"; and 3) Presentation Slides on the Full Year 2017 Results. Additional Details For Financial Period Ended 31/12/2017 Attachments CDL_FY2017_Results.pdf CDL_NewsRelease-Q4andFY2017Results.pdf CDL_FY2017_Results_Presentation.pdf Total size =4076K

Page 1 of 1 Financial Statements and Related Announcement::Full Yearly Results 2/28/2018 http://infopub.sgx.com/Apps?A=COW_CorpAnnouncement_Content&B...