SLIDE 1

2/7/2009 1

Economic Crisis Economic Crisis and and A Strategy A Strategy

A K Chaudhuri A K Chaudhuri

Director, ADAAP Process Solutions Pvt. Ltd. Director, ADAAP Process Solutions Pvt. Ltd. Visiting Faculty, Indian Statistical Institute Visiting Faculty, Indian Statistical Institute & Chairman, National Institution for Quality & Reliability, Chairman, National Institution for Quality & Reliability, Bangalore Bangalore

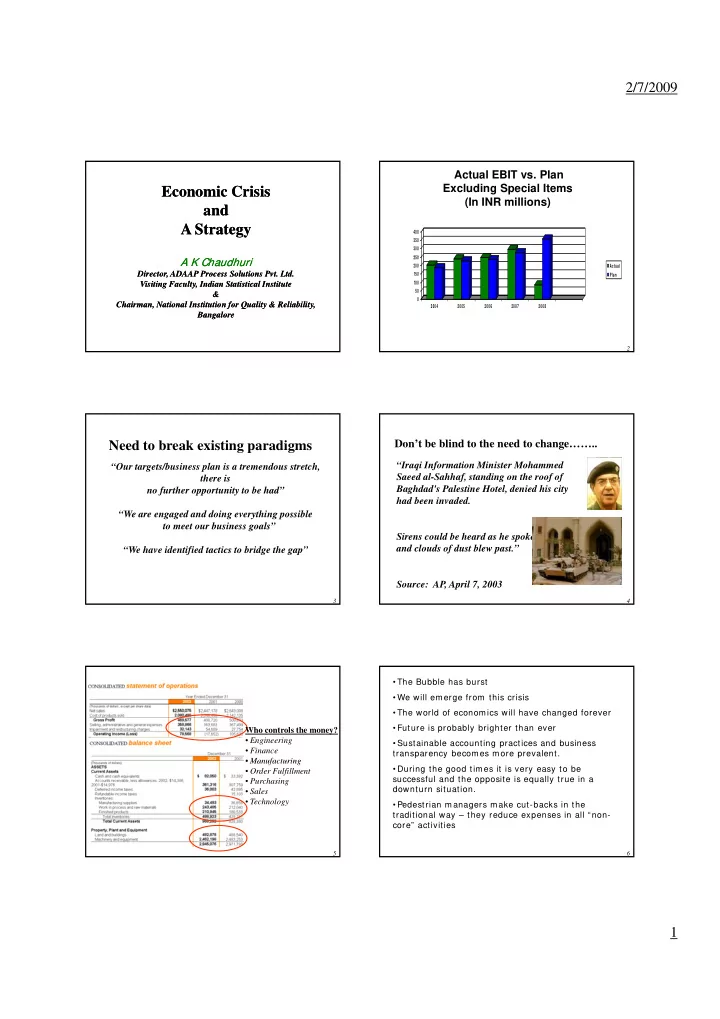

Actual EBIT vs. Plan Excluding Special Items (In INR millions)

250 300 350 400

2

50 100 150 200 250 2004 2005 2006 2007 2008 Actual Plan

“Our targets/business plan is a tremendous stretch, there is no further opportunity to be had”

Need to break existing paradigms

3

“We are engaged and doing everything possible to meet our business goals” “We have identified tactics to bridge the gap”

Don’t be blind to the need to change……..

“Iraqi Information Minister Mohammed Saeed al-Sahhaf, standing on the roof of Baghdad's Palestine Hotel, denied his city had been invaded.

4

Sirens could be heard as he spoke and clouds of dust blew past.” Source: AP, April 7, 2003

Who controls the money?

- Engineering

- Finance

- Manufacturing

5

- Manufacturing

- Order Fulfillment

- Purchasing

- Sales

- Technology

- The Bubble has burst

- We will emerge from this crisis

- The world of economics will have changed forever

- Future is probably brighter than ever

- Sustainable accounting practices and business

transparency becomes more prevalent.

6

- During the good times it is very easy to be

successful and the opposite is equally true in a downturn situation.

- Pedestrian managers make cut-backs in the

traditional way – they reduce expenses in all “non- core” activities