1

- Dr. Edward Altman

NYU Stern School of Business

Current Conditions & Outlook in Credit Markets

A Tale of Three Periods

Distressed Assets Symposium University of Toronto Faculty of Law Toronto, Canada March 03, 2010

2

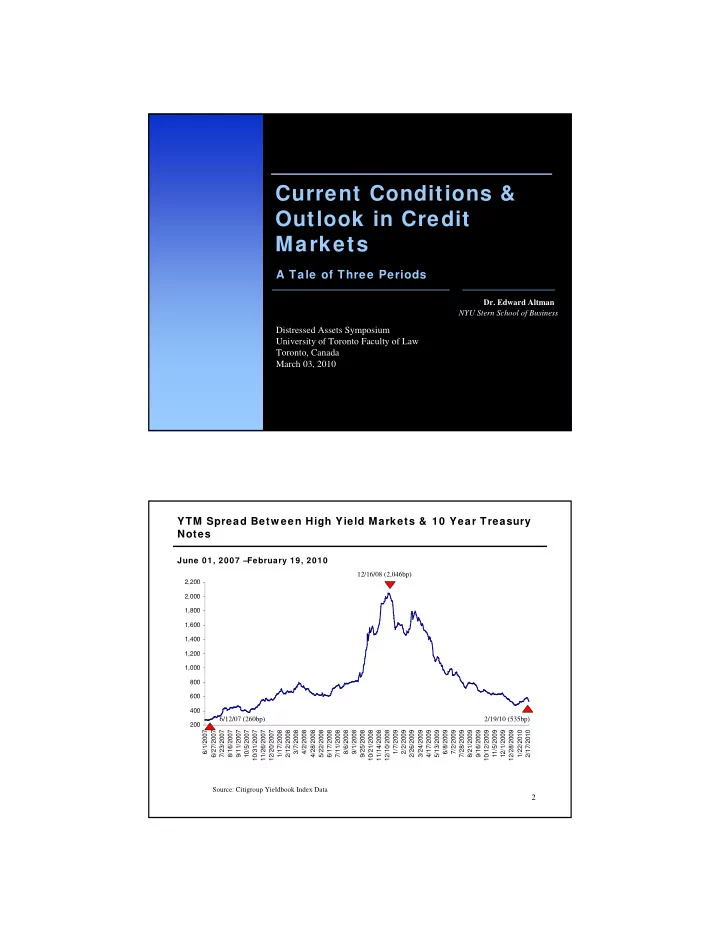

YTM Spread Betw een High Yield Markets & 10 Year Treasury Notes

June 01, 2007 –February 19, 2010

Source: Citigroup Yieldbook Index Data

200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000 2,200 6/1/2007 6/27/2007 7/23/2007 8/16/2007 9/11/2007 10/5/2007 10/31/2007 11/26/2007 12/20/2007 1/17/2008 2/12/2008 3/7/2008 4/2/2008 4/28/2008 5/22/2008 6/17/2008 7/11/2008 8/6/2008 9/1/2008 9/25/2008 10/21/2008 11/14/2008 12/10/2008 1/7/2009 2/2/2009 2/26/2009 3/24/2009 4/17/2009 5/13/2009 6/8/2009 7/2/2009 7/28/2009 8/21/2009 9/16/2009 10/12/2009 11/5/2009 12/1/2009 12/28/2009 1/22/2010 2/17/2010

6/12/07 (260bp) 12/16/08 (2,046bp) 2/19/10 (535bp)