SLIDE 1

ECO 305 — FALL 2003 — September 23

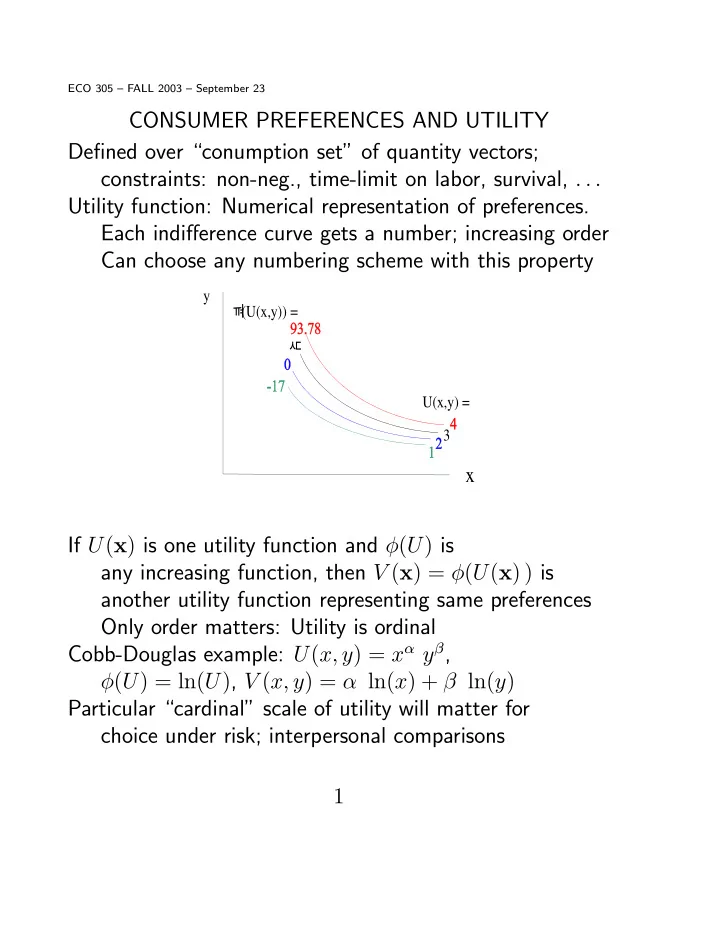

CONSUMER PREFERENCES AND UTILITY Defined over “conumption set” of quantity vectors; constraints: non-neg., time-limit on labor, survival, . . . Utility function: Numerical representation of preferences. Each indifference curve gets a number; increasing order Can choose any numbering scheme with this property

x

y U(x,y) = 3 N (U(x,y)) = B

If U(x) is one utility function and φ(U) is any increasing function, then V (x) = φ(U(x) ) is another utility function representing same preferences Only order matters: Utility is ordinal Cobb-Douglas example: U(x, y) = xα yβ, φ(U) = ln(U), V (x, y) = α ln(x) + β ln(y) Particular “cardinal” scale of utility will matter for choice under risk; interpersonal comparisons 1

SLIDE 2

FORMAL STATEMENT: Notation: Preferred x  y, Indifferent x ∼ y Requirements of rationality: (1) Complete: for any x, y, x  y or y  x or x ∼ y (2) Reflexive: for any x, x ∼ x (3) Transitive: If x  y and y  z, then x  z (4) Continuous: If x  y and z “near” y, then x  z Theorem: These there imply that there is a function U such that U(x) > U(y) if and only if x  y. MARGINAL RATE OF SUBSTITUTION Solve u = U(x, y) to get y = f(x, u). (Numerical) slope MRSyx = − dy dx

¯ ¯ ¯ ¯ ¯

U=constant

= ∂U/∂x ∂U/∂y MRS independent of cardinal utility: If V (x, y) = φ(U(x, y) ), ∂V/∂x ∂V/∂y = φ0(U) ∂U/∂x φ0(U) ∂U/∂y = ∂U/∂x ∂U/∂y Diminishing MRS: As x ↑ and y ↓ holding U constant, MRS decreases (indifference curve becomes flatter). SOSC for utility max subject to linear budget constraint Equivalent statement — If x ∼ y, then 1

2(x + y) Â x, y

2

SLIDE 3

UTILITY MAXIMIZATION To maximize U(x, y) subject to Px x + Py y ≤ M. Budget constraint will be binding if “non-satiation” Lagrange FONCs for interior maximum L(x, y) = U(x, y) + λ [M − Px x − Py y] ∂L/∂x = ∂U/∂x − λ Px = 0 ∂L/∂y = ∂U/∂y − λ Py = 0 INTERPRETATIONS If (x∗, y∗) are optimum qunatities and u∗ = U(x∗, y∗), then λ = du∗/dM, “marginal utility of money” An extra dollar of income will buy you either 1/Px of x or 1/Py of y Respective utility increments from these are ∂U/∂x Px and ∂U/∂y Py Equal because of optimization; common value is the extra utility yielded by the extra dollar λ Px is “marginal (utility) cost” of buying x FONC: marginal (utility) benefit - marginal cost = 0 3

SLIDE 4

FONC for boundary optimum (0, y∗) ∂L/∂x = ∂U/∂x − λ Px ≤ 0 ∂L/∂y = ∂U/∂y − λ Py = 0 ∂U/∂x Px ≤ ∂U/∂y Py = λ Last dollar spent on y yields utility (∂U/∂y)/Py = λ First dollar spent on x would yield (∂U/∂x)/Px, less (GENERALIZED) DEMAND FUNCTIONS Optimum quantity choices x = Dx(Px, Py, M), y = Dy(Px, Py, M) Marshallian or uncompensated or gross demand functions Simplest properties: (1) Adding up: Px Dx(Px, Py, M)+Py Dy(Px, Py, M) ≡ M (2) Homogeneity of degree zero: Dx(k Px, k Py, k M) = Dx(Px, Py, M) Budget constraint unaffected; no money illusion (3) Don’t depend on cardinal utility: If V (x, y) = φ(U(x, y) ), and µ is Lagrange multiplier when maxing V (x, y), ∂V/∂x = µ Px, ∂V/∂y = µ Py φ0(U) ∂U/∂x = µ Px, φ0(U) ∂U/∂y = µ Py same as FONCs for maxing U(x, y) with µ/φ0(U) = λ 4

SLIDE 5

COBB-DOUGLAS EXAMPLE To max U(x, y) = xα yβ, FONCs are ∂U/∂x ≡ α xα−1 yβ = λ Px, ∂U/∂y ≡ β xα yβ−1 = λ Py Px x α = Py y β = xα yβ λ M = Px x + Py y = (α + β) xα yβ λ Px x α = Py y β = M α + β Px x M = α α + β, Py y M = β α + β Proportions or shares of income spent on the two goods are constants. Check: (1) No boundary optima: U(0, y) = U(x, 0) = 0 whereas U(x, y) > 0 when both x, y are positive. (2) Second Order Conditions: Indifference curves convex: xα yβ = u, y = u1/β x−α/β Exercise: Use V (x, y) = α ln(x) + β ln(y) and find (1) same demand functions; (2) relation between multipliers 5

SLIDE 6

Income-Consumption Curve: Price-Consumption Curve:

x y x y

Algebraic concepts: Income elasticity: ∆x / x ∆M / M → M x ∂x ∂M Own Price elasticity: ∆x / x ∆Px / Px → Px x ∂x ∂Px Cross-Price elasticity: ∆x / x ∆Py / Py → Py x ∂x ∂Py Income elasticity < 0: inferior, > 0: normal, > 1: luxury between 0 and 1: necessity Own Price elasticity > 0: Giffen Cross-price elasticity > 0: Marshallian or gross substitues < 0: Marshallian or gross complements General concept : Comparative statics 6