SLIDE 1

Cenovus delivers strong second quarter perform ance

Planned divestitures and Deep Basin asset integration on track

Calgary, Alberta ( July 2 7 , 2 0 1 7 ) – Cenovus Energy Inc. (TSX: CVE) (NYSE: CVE) had a strong second quarter that reflected 45 days of results from the assets recently acquired from ConocoPhillips. The acquisition gives Cenovus 100% ownership of its oil sands operations and a new production platform in the liquids-rich Deep Basin. Integration of the Deep Basin assets is on track. To further optimize its portfolio and deleverage its balance sheet, the company is pursuing the sale of its legacy conventional oil and natural gas assets, and the sale processes are proceeding well. Cenovus continues to target between $4 billion and $5 billion in announced asset sale agreements during 2017. Key highlights Increased second quarter adjusted funds flow by 80% to $792 million or $0.71 per share compared with the same period in 2016 Increased free funds flow by 128% from the second quarter of 2016 to $465 million Reduced planned 2017 capital spending by approximately $200 million to $1.7 billion at the midpoint, with no expected impact to forecast production volumes

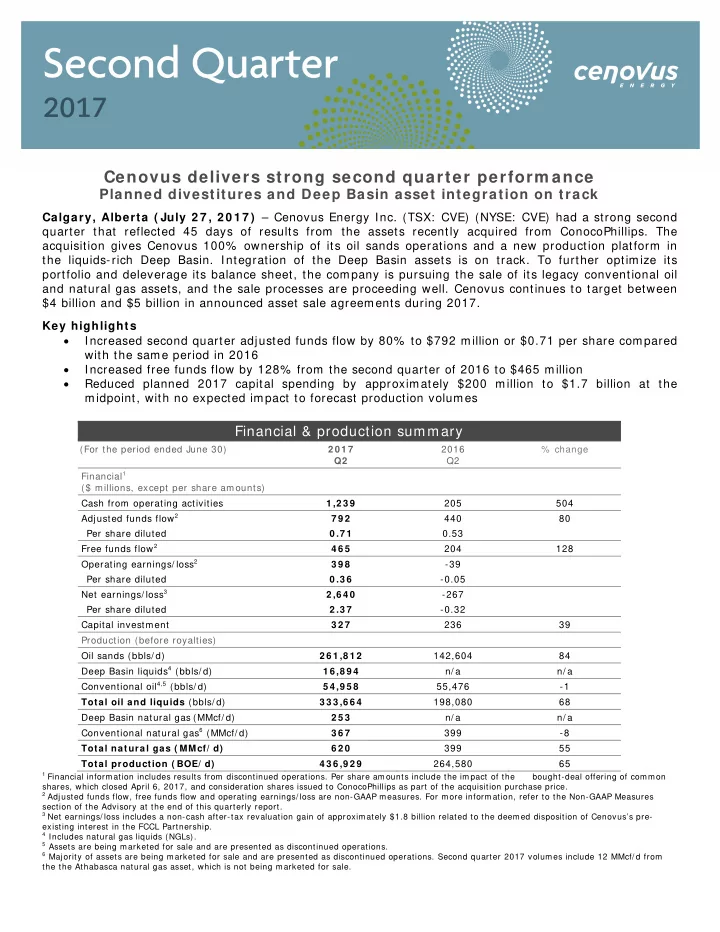

Financial & production summary

(For the period ended June 30) 2 0 1 7 Q2 2016 Q2 % change Financial1 ($ millions, except per share amounts) Cash from operating activities 1 ,2 3 9 205 504 Adjusted funds flow2 7 9 2 440 80 Per share diluted 0 .7 1 0.53 Free funds flow 2 4 6 5 204 128 Operating earnings/ loss2 3 9 8

- 39

Per share diluted 0 .3 6

- 0.05

Net earnings/ loss3 2 ,6 4 0

- 267

Per share diluted 2 .3 7

- 0.32

Capital investment 3 2 7 236 39 Production (before royalties) Oil sands (bbls/ d) 2 6 1 ,8 1 2 142,604 84 Deep Basin liquids4 (bbls/ d) 1 6 ,8 9 4 n/ a n/ a Conventional oil4,5 (bbls/ d) 5 4 ,9 5 8 55,476

- 1

Total oil and liquids (bbls/ d) 3 3 3 ,6 6 4 198,080 68 Deep Basin natural gas (MMcf/ d) 2 5 3 n/ a n/ a Conventional natural gas6 (MMcf/ d) 3 6 7 399

- 8

Total natural gas ( MMcf/ d) 6 2 0 399 55 Total production ( BOE/ d) 4 3 6 ,9 2 9 264,580 65

1 Financial information includes results from discontinued operations. Per share amounts include the impact of the bought-deal offering of common

shares, which closed April 6, 2017, and consideration shares issued to ConocoPhillips as part of the acquisition purchase price.

2 Adjusted funds flow, free funds flow and operating earnings/ loss are non-GAAP measures. For more information, refer to the Non-GAAP Measures

section of the Advisory at the end of this quarterly report.

3 Net earnings/ loss includes a non-cash after-tax revaluation gain of approximately $1.8 billion related to the deemed disposition of Cenovus’s pre-

existing interest in the FCCL Partnership.

4 Includes natural gas liquids (NGLs). 5 Assets are being marketed for sale and are presented as discontinued operations. 6 Majority of assets are being marketed for sale and are presented as discontinued operations. Second quarter 2017 volumes include 12 MMcf/ d from