SLIDE 1

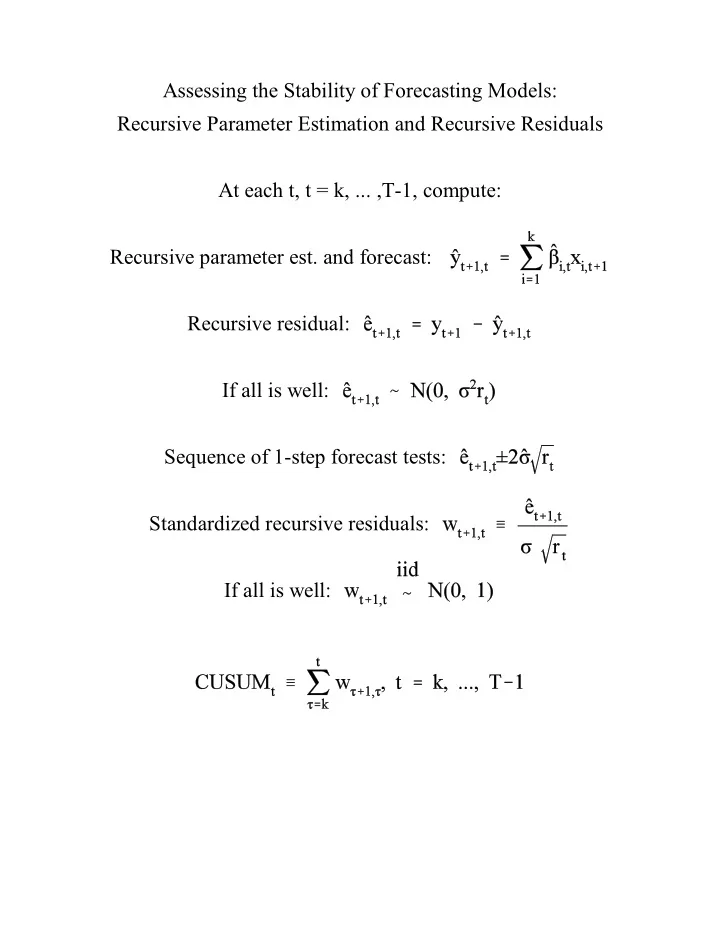

Assessing the Stability of Forecasting Models: Recursive Parameter Estimation and Recursive Residuals At each t, t = k, ... ,T-1, compute: Recursive parameter est. and forecast: Recursive residual: If all is well: Sequence of 1-step forecast tests: Standardized recursive residuals: If all is well:

SLIDE 2

Recursive Analysis Constant Parameter Model

SLIDE 3

Recursive Analysis Breaking Parameter Model

SLIDE 4

Log Liquor Sales Quadratic Trend Regression with Seasonal Dummies and AR(3) Disturbances Recursive Residuals and Two Standard Error Bands

SLIDE 5

Distributed Lags Start with unconditional forecasting model: Generalize to “distributed lag model” “lag weights” “lag distribution”

SLIDE 6

Another way: distributed lag regression with lagged dependent variables Another way: distributed lag regression with ARMA disturbances

SLIDE 7

Vector Autoregressions e.g., bivariate VAR(1) Estimation by OLS Order selection by information criteria Impulse-response functions, variance decompositions, predictive causality Forecasts via Wold’s chain rule

SLIDE 8

U.S. Housing Starts and Completions, 1968.01 - 1996.06 Notes to figure: The left scale is starts, and the right scale is completions.

SLIDE 9 Starts Correlogram Sample: 1968:01 1991:12 Included observations: 288 Acorr.

Ljung-Box p-value 1 0.937 0.937 0.059 255.24 0.000 2 0.907 0.244 0.059 495.53 0.000 3 0.877 0.054 0.059 720.95 0.000 4 0.838

0.059 927.39 0.000 5 0.795

0.059 1113.7 0.000 6 0.751

0.059 1280.9 0.000 7 0.704

0.059 1428.2 0.000 8 0.650

0.059 1554.4 0.000 9 0.604 0.004 0.059 1663.8 0.000 10 0.544

0.059 1752.6 0.000 11 0.496 0.029 0.059 1826.7 0.000 12 0.446

0.059 1886.8 0.000 13 0.405 0.076 0.059 1936.8 0.000 14 0.346

0.059 1973.3 0.000 15 0.292

0.059 1999.4 0.000 16 0.233

0.059 2016.1 0.000 17 0.175

0.059 2025.6 0.000 18 0.122

0.059 2030.2 0.000 19 0.070 0.002 0.059 2031.7 0.000 20 0.019

0.059 2031.8 0.000 21

0.059 2032.2 0.000 22

0.036 0.059 2033.9 0.000 23

0.059 2038.7 0.000 24

0.059 2047.4 0.000

SLIDE 10

Starts Sample Autocorrelations and Partial Autocorrelations

SLIDE 11 Completions Correlogram Sample: 1968:01 1991:12 Included observations: 288 Acorr.

Ljung-Box p-value 1 0.939 0.939 0.059 256.61 0.000 2 0.920 0.328 0.059 504.05 0.000 3 0.896 0.066 0.059 739.19 0.000 4 0.874 0.023 0.059 963.73 0.000 5 0.834

0.059 1168.9 0.000 6 0.802

0.059 1359.2 0.000 7 0.761

0.059 1531.2 0.000 8 0.721

0.059 1686.1 0.000 9 0.677

0.059 1823.2 0.000 10 0.633

0.059 1943.7 0.000 11 0.583

0.059 2046.3 0.000 12 0.533

0.059 2132.2 0.000 13 0.483

0.059 2203.2 0.000 14 0.434

0.059 2260.6 0.000 15 0.390 0.041 0.059 2307.0 0.000 16 0.337

0.059 2341.9 0.000 17 0.290

0.059 2367.9 0.000 18 0.234

0.059 2384.8 0.000 19 0.181

0.059 2395.0 0.000 20 0.128

0.059 2400.1 0.000 21 0.068

0.059 2401.6 0.000 22 0.020 0.037 0.059 2401.7 0.000 23

0.059 2402.2 0.000 24

0.059 2404.6 0.000

SLIDE 12

Completions Sample Autocorrelations and Partial Autocorrelations

SLIDE 13

Starts and Completions Sample Cross Correlations Notes to figure: We graph the sample correlation between completions at time t and starts at time t-i, i = 1, 2, ..., 24.

SLIDE 14 VAR Starts Equation LS // Dependent Variable is STARTS Sample(adjusted): 1968:05 1991:12 Included observations: 284 after adjusting endpoints Variable Coefficient

t-Statistic Prob. C 0.146871 0.044235 3.320264 0.0010 STARTS(-1) 0.659939 0.061242 10.77587 0.0000 STARTS(-2) 0.229632 0.072724 3.157587 0.0018 STARTS(-3) 0.142859 0.072655 1.966281 0.0503 STARTS(-4) 0.007806 0.066032 0.118217 0.9060 COMPS(-1) 0.031611 0.102712 0.307759 0.7585 COMPS(-2)

0.103847

0.2458 COMPS(-3)

0.100946

0.8384 COMPS(-4)

0.094569

0.7722 R-squared 0.895566 Mean dependent var 1.574771 Adjusted R-squared 0.892528 S.D. dependent var 0.382362 S.E. of regression 0.125350 Akaike info criterion

Sum squared resid 4.320952 Schwarz criterion

Log likelihood 191.3622 F-statistic 294.7796 Durbin-Watson stat 1.991908 Prob(F-statistic) 0.000000

SLIDE 15

VAR Starts Equation Residual Plot

SLIDE 16 VAR Starts Equation Residual Correlogram Sample: 1968:01 1991:12 Included observations: 284 Acorr.

Ljung-Box p-value 1 0.001 0.001 0.059 0.0004 0.985 2 0.003 0.003 0.059 0.0029 0.999 3 0.006 0.006 0.059 0.0119 1.000 4 0.023 0.023 0.059 0.1650 0.997 5

0.059 0.2108 0.999 6 0.022 0.021 0.059 0.3463 0.999 7 0.038 0.038 0.059 0.7646 0.998 8

0.059 1.4362 0.994 9 0.056 0.056 0.059 2.3528 0.985 10

0.059 6.1868 0.799 11

0.059 6.6096 0.830 12

0.059 6.8763 0.866 13 0.192 0.193 0.059 17.947 0.160 14 0.014 0.021 0.059 18.010 0.206 15 0.063 0.067 0.059 19.199 0.205 16

0.059 19.208 0.258 17

0.059 19.664 0.292 18

0.059 19.927 0.337 19

0.059 19.959 0.397 20 0.010

0.059 19.993 0.458 21

0.059 21.003 0.459 22 0.045 0.018 0.059 21.644 0.481 23

0.011 0.059 22.088 0.515 24

0.059 29.064 0.218

SLIDE 17

VAR Starts Equation Residual Sample Autocorrelations and Partial Autocorrelations

SLIDE 18 VAR Completions Equation LS // Dependent Variable is COMPS Sample(adjusted): 1968:05 1991:12 Included observations: 284 after adjusting endpoints Variable Coefficient

t-Statistic Prob. C 0.045347 0.025794 1.758045 0.0799 STARTS(-1) 0.074724 0.035711 2.092461 0.0373 STARTS(-2) 0.040047 0.042406 0.944377 0.3458 STARTS(-3) 0.047145 0.042366 1.112805 0.2668 STARTS(-4) 0.082331 0.038504 2.138238 0.0334 COMPS(-1) 0.236774 0.059893 3.953313 0.0001 COMPS(-2) 0.206172 0.060554 3.404742 0.0008 COMPS(-3) 0.120998 0.058863 2.055593 0.0408 COMPS(-4) 0.156729 0.055144 2.842160 0.0048 R-squared 0.936835 Mean dependent var 1.547958 Adjusted R-squared 0.934998 S.D. dependent var 0.286689 S.E. of regression 0.073093 Akaike info criterion

Sum squared resid 1.469205 Schwarz criterion

Log likelihood 344.5453 F-statistic 509.8375 Durbin-Watson stat 2.013370 Prob(F-statistic) 0.000000

SLIDE 19

VAR Completions Equation Residual Plot

SLIDE 20 VAR Completions Equation Residual Correlogram Sample: 1968:01 1991:12 Included observations: 284 Acorr.

Ljung-Box p-value 1

0.059 0.0238 0.877 2

0.059 0.3744 0.829 3

0.059 0.7640 0.858 4

0.059 3.0059 0.557 5

0.059 6.1873 0.288 6 0.012 0.000 0.059 6.2291 0.398 7

0.059 6.4047 0.493 8 0.041 0.024 0.059 6.9026 0.547 9 0.048 0.029 0.059 7.5927 0.576 10 0.045 0.037 0.059 8.1918 0.610 11

0.059 8.2160 0.694 12

0.059 8.9767 0.705 13

0.059 9.4057 0.742 14

0.059 10.318 0.739 15 0.027 0.028 0.059 10.545 0.784 16

0.059 10.553 0.836 17 0.096 0.082 0.059 13.369 0.711 18 0.011

0.059 13.405 0.767 19 0.041 0.040 0.059 13.929 0.788 20 0.046 0.061 0.059 14.569 0.801 21

0.059 17.402 0.686 22 0.039 0.077 0.059 17.875 0.713 23

0.059 21.824 0.531 24

0.059 27.622 0.276

SLIDE 21

VAR Completions Equation Residual Sample Autocorrelations and Partial Autocorrelations

SLIDE 22

Housing Starts and Completions Causality Tests Sample: 1968:01 1991:12 Lags: 4 Obs: 284 Null Hypothesis: F-Statistic Probability STARTS does not Cause COMPS 26.2658 0.00000 COMPS does not Cause STARTS 2.23876 0.06511

SLIDE 23

Starts History, 1968.01-1991.12 Forecast, 1992.01-1996.06

SLIDE 24

Starts History, 1968.01-1991.12 Forecast and Realization, 1992.01-1996.06

SLIDE 25

Completions History, 1968.01-1991.12 Forecast, 1992.01-1996.06

SLIDE 26

Completions History, 1968.01-1991.12 Forecast and Realization, 1992.01-1996.06

SLIDE 27

Random walk: Random walk with drift: Stochastic trend vs deterministic trend

SLIDE 28

Properties of random walks With time 0 value :

SLIDE 29

Random Walk Level and Change

SLIDE 30

Random walk with drift Assuming time 0 value :

SLIDE 31

Random Walk With Drift Level and Change

SLIDE 32

Random walk example Point forecast Recall that for the AR(1) process, the optimal forecast is Thus in the random walk case,

SLIDE 33 Effects of Unit Roots Sample autocorrelation function “fails to damp” Sample partial autocorrelation function near 1 for , and then damps quickly Properties of estimators change e.g., least-squares autoregression with unit roots True process: Estimated model: Superconsistency: stabilizes as sample size grows Bias:

- - Ofsetting effects of bias and superconsistency

SLIDE 34

Unit Root Tests “Dickey-Fuller distribution” Trick regression:

SLIDE 35

Allowing for nonzero mean under the alternative Basic model: which we rewrite as where á vanishes when (null) á is nevertheless present under the alternative, so we include an intercept in the regression Dickey-Fuller distribution

SLIDE 36 Allowing for deterministic linear trend under the alternative Basic model:

where and . Under the null hypothesis we have a random walk with drift, Under the deterministic-trend alternative hypothesis both the intercept and the trend enter and so are included in the regression.

SLIDE 37

U.S. Per Capita GNP History and Two Forecasts

SLIDE 38

U.S. Per Capita GNP History, Two Forecasts, and Realization

SLIDE 39

Allowing for higher-order autoregressive dynamics AR(p) process: Rewrite: where , , and , . Unit root: (AR(p-1) in first differences) distribution holds asymptotically