SLIDE 1

ADDITIONAL RESOURCES ON REVENUE IDEAS FOR THE TEXAS EDUCATION - - PDF document

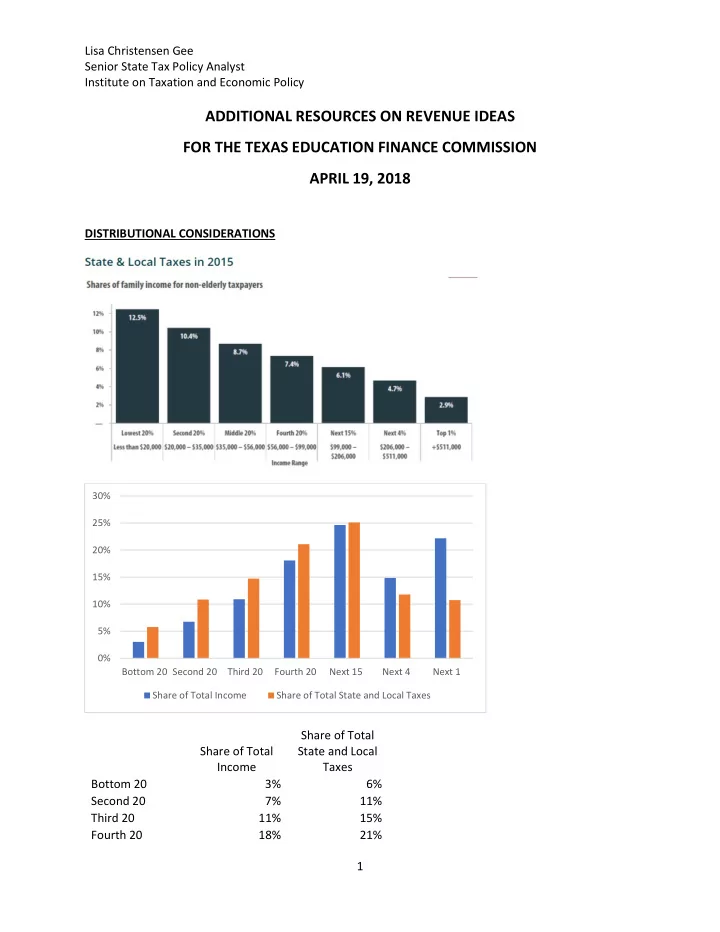

Lisa Christensen Gee Senior State Tax Policy Analyst Institute on Taxation and Economic Policy ADDITIONAL RESOURCES ON REVENUE IDEAS FOR THE TEXAS EDUCATION FINANCE COMMISSION APRIL 19, 2018 DISTRIBUTIONAL CONSIDERATIONS 30% 25% 20% 15%