SLIDE 1

1

JOHAN DENNELIND PRESIDENT & CEO

YEAR-END REPORT JANUARY – DECEMBER 2018

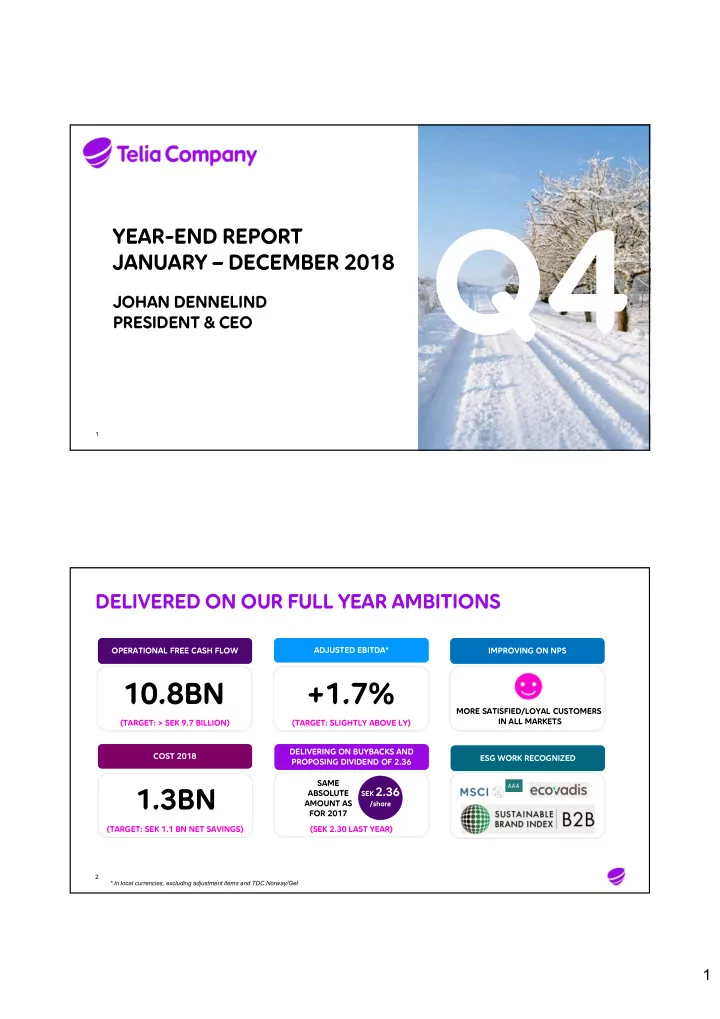

1DELIVERED ON OUR FULL YEAR AMBITIONS

OPERATIONAL FREE CASH FLOW OPERATIONAL FREE CASH FLOW COST 2018 COST 2018 DELIVERING ON BUYBACKS AND PROPOSING DIVIDEND OF 2.36 DELIVERING ON BUYBACKS AND PROPOSING DIVIDEND OF 2.36 ADJUSTED EBITDA* ADJUSTED EBITDA*1.3BN

10.8BN

SEK 2.36 /share+1.7%

(TARGET: > SEK 9.7 BILLION) (TARGET: SLIGHTLY ABOVE LY) (TARGET: SEK 1.1 BN NET SAVINGS) (SEK 2.30 LAST YEAR) * In local currencies, excluding adjustment items and TDC Norway/Get SAME ABSOLUTE AMOUNT AS FOR 2017 ESG WORK RECOGNIZED ESG WORK RECOGNIZED IMPROVING ON NPS IMPROVING ON NPS MORE SATISFIED/LOYAL CUSTOMERS IN ALL MARKETS 2