iW PARTNERS

asset management - asset services - asset solutions

FOR PROFESSIONAL CLIENTS/WELL-INFORMED INVESTORS ONLY - NOT FOR RETAIL USE OR DISTRIBUTION

INVESTMENT OBJECTIVE

Seek an annualized positjve performance above EONIA1 in- fmatjon adjusted2 over its recommended minimum holding period of 3 years through the selectjon of specialized fund managers within a dynamic and fmexible allocatjon to alter- natjve investment strategies.

1 EONIA : Euro Overnight Index Average (a short term money market reference rate for the euro) 2 Infmatjon adjusted : Monthly infmatjon fjgures are taken from the Harmonised Index of Consumer Prices for the European Union

Equity Hedge

; ; Long/Short Equity ; ; Long/Short Credit ; ; Short Bias ; ; Convertjble Bonds ; ; …

Relatjve Value

; ; Equity Market Neutral ; ; Fixed Income Arbitrage ; ; Convertjble Arbitrage ; ; …

Global Assets

; ; Global Macro ; ; CTA/Managed Futures ; ; Emerging Market ; ; …

Event Driven

; ; Merger Arbitrage ; ; Distressed Securitjes ; ; Actjvist Shareholder ; ; Special Situatjons ; ; …

FUND HIGHLIGHTS

- Optjmized risk return allocatjon to alternatjve strategies,

low correlatjon to traditjonal asset classes

- Focus on independent managers who have demonstrated

best-in-class skills in various market conditjons

- Target Performance : EONIA1 infmatjon adjusted2

- Experienced investment team in open architecture plat-

forms

WHY ALTERNATIVE STRATEGIES INVESTMENT THESIS

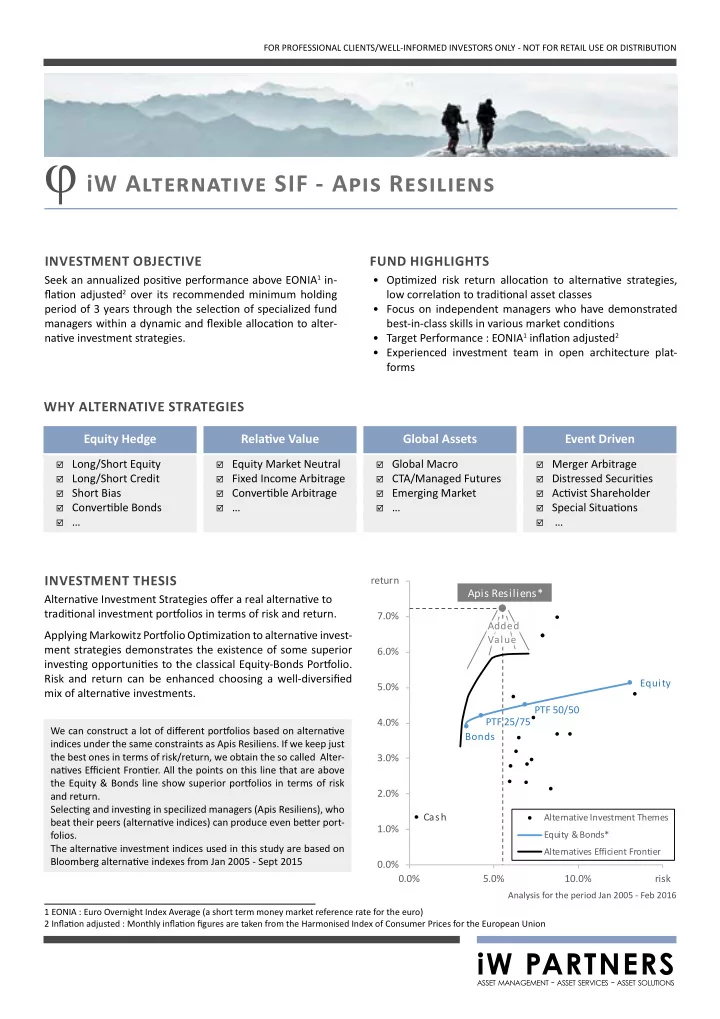

Alternatjve Investment Strategies ofger a real alternatjve to traditjonal investment portgolios in terms of risk and return. Applying Markowitz Portgolio Optjmizatjon to alternatjve invest- ment strategies demonstrates the existence of some superior investjng opportunitjes to the classical Equity-Bonds Portgolio. Risk and return can be enhanced choosing a well-diversifjed mix of alternatjve investments.

We can construct a lot of difgerent portgolios based on alternatjve indices under the same constraints as Apis Resiliens. If we keep just the best ones in terms of risk/return, we obtain the so called Alter- natjves Effjcient Frontjer. All the points on this line that are above the Equity & Bonds line show superior portgolios in terms of risk and return. Selectjng and investjng in specilized managers (Apis Resiliens), who beat their peers (alternatjve indices) can produce even betuer port- folios. The alternatjve investment indices used in this study are based on Bloomberg alternatjve indexes from Jan 2005 - Sept 2015

Analysis for the period Jan 2005 - Feb 2016

Apis Resiliens*

Cash Bonds PTF 25/75 PTF 50/50 Equity 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% return 0.0% 5.0% 10.0% risk

Alternative Investment Themes Equity & Bonds* Alternatives Efficient Frontier

Added Value