SLIDE 1

1

JOHAN DENNELIND PRESIDENT & CEO

INTERIM REPORT JANUARY – MARCH 2018

Q1

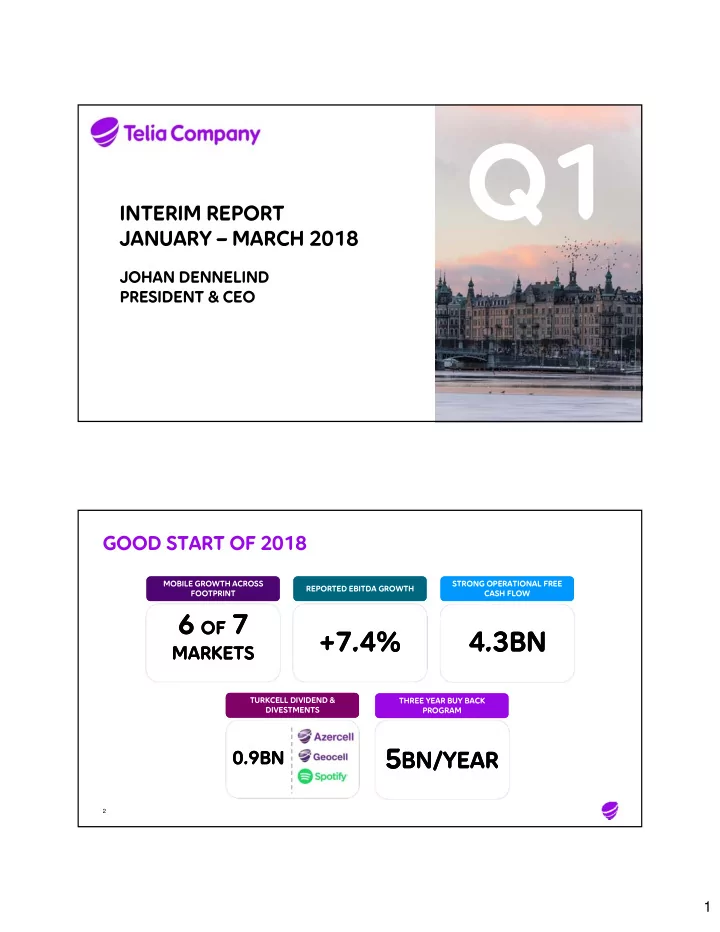

GOOD START OF 2018

2 MOBILE GROWTH ACROSS FOOTPRINT MOBILE GROWTH ACROSS FOOTPRINT TURKCELL DIVIDEND & DIVESTMENTS TURKCELL DIVIDEND & DIVESTMENTS THREE YEAR BUY BACK PROGRAM THREE YEAR BUY BACK PROGRAM STRONG OPERATIONAL FREE CASH FLOW STRONG OPERATIONAL FREE CASH FLOW6 OF 7

MARKETS

6 OF 7

MARKETS

5BN/YEAR 5BN/YEAR

0.9BN 0.9BN

4.3BN 4.3BN

REPORTED EBITDA GROWTH REPORTED EBITDA GROWTH+7.4% +7.4%