SLIDE 1

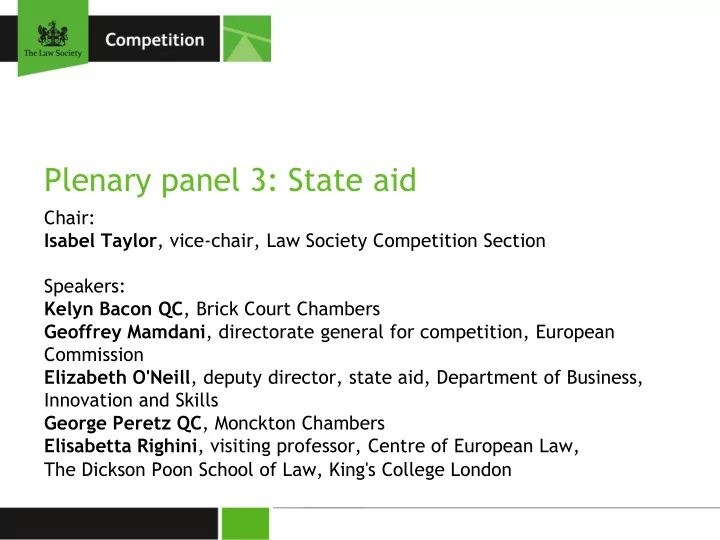

Plenary panel 3: State aid

Chair: Isabel Taylor, vice-chair, Law Society Competition Section Speakers: Kelyn Bacon QC, Brick Court Chambers Geoffrey Mamdani, directorate general for competition, European Commission Elizabeth O'Neill, deputy director, state aid, Department of Business, Innovation and Skills George Peretz QC, Monckton Chambers Elisabetta Righini, visiting professor, Centre of European Law, The Dickson Poon School of Law, King's College London