SLIDE 1

Overview of HHR Spending

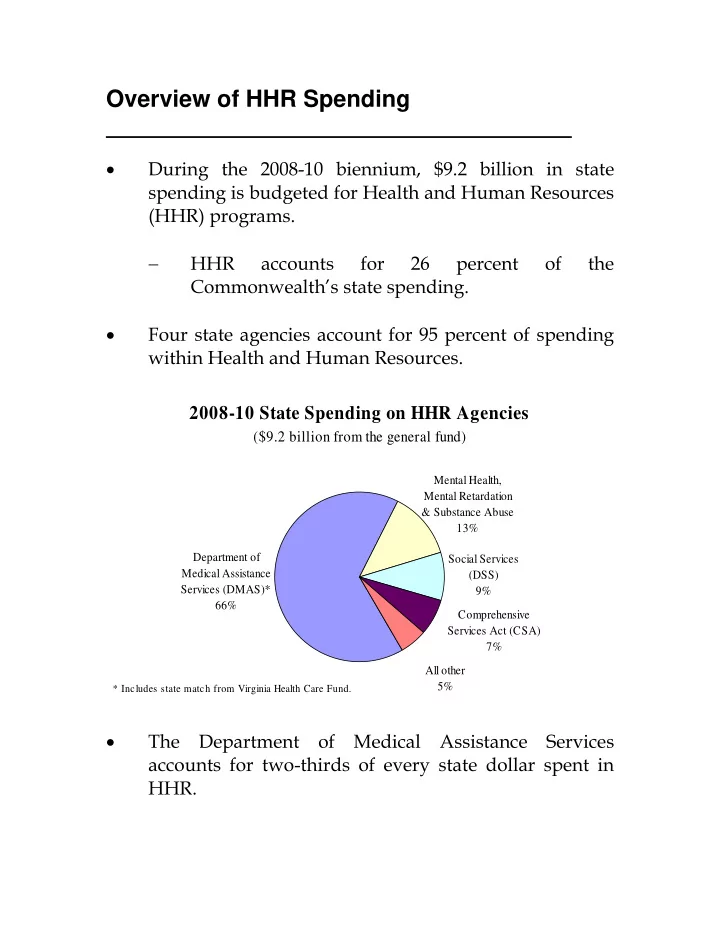

- During the 2008-10 biennium, $9.2 billion in state

spending is budgeted for Health and Human Resources (HHR) programs. − HHR accounts for 26 percent

- f

the Commonwealth’s state spending.

- Four state agencies account for 95 percent of spending

within Health and Human Resources. 2008-10 State Spending on HHR Agencies

($9.2 billion from the general fund)

Department of Medical Assistance Services (DMAS)* 66% Social Services (DSS) 9% Comprehensive Services Act (CSA) 7% All other 5% Mental Health, Mental Retardation & Substance Abuse 13%

* Includes state match from Virginia Health Care Fund.

- The Department of Medical Assistance Services