SLIDE 1

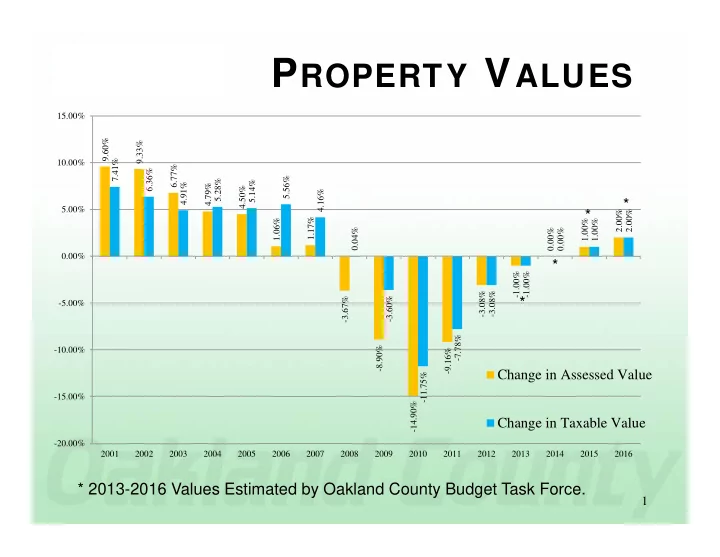

PROPERTY VALUES

1

9.60% 9.33% 6.77% 4.79% 4.50% 1.06% 1.17%

- 3.67%

- 8.90%

- 14.90%

- 9.16%

- 3.08%

- 1.00%

0.00% 1.00% 2.00% 7.41% 6.36% 4.91% 5.28% 5.14% 5.56% 4.16% 0.04%

- 3.60%

- 11.75%

- 7.78%

- 3.08%

- 1.00%

0.00% 1.00% 2.00%

- 20.00%

- 15.00%

- 10.00%

- 5.00%

0.00% 5.00% 10.00% 15.00% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Change in Assessed Value Change in Taxable Value

* 2013-2016 Values Estimated by Oakland County Budget Task Force. * * * *