SLIDE 1

New Methods for Time Series and Panel Econometrics

Peter C. B. Phillips Cowles Foundation, Yale University

IMF Seminar: September 29, 2003

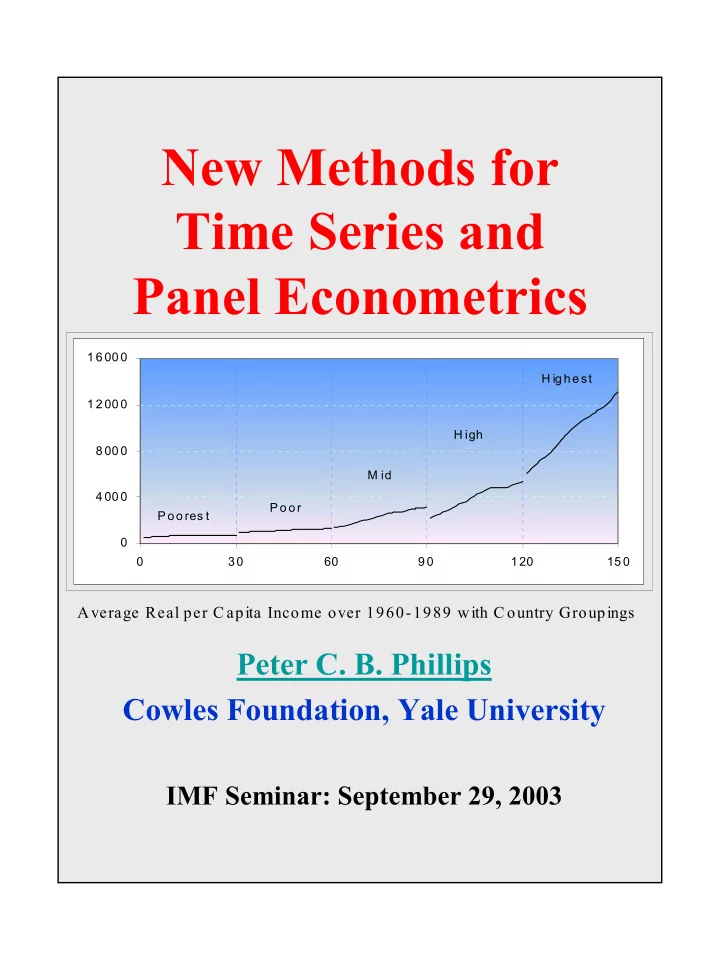

4 00 0 8 00 0 1 2 00 0 1 6 00 0 3 0 60 9 0 1 20 15 0 Po o res t Po o r M id H igh H ig h e st

Average Real per C apita Income over 1960-1989 with C ountry Groupings