SLIDE 1

6/11/2014 1

Cheap but Flighty: Global Imbalances and Bank Instability

Toni Ahnert

Bank of Canada

Enrico Perotti

University of Amsterdam

Macro explanations for the crisis

- Popular views: the crisis was caused by

– low interest rates (Fed policy), or – the accumulation of global imbalances.

- No clear foundations.

- The US credit boom was not funded by the

Fed, but by capital markets.

- Major role for capital inflows from EM

countries; may explain low rates

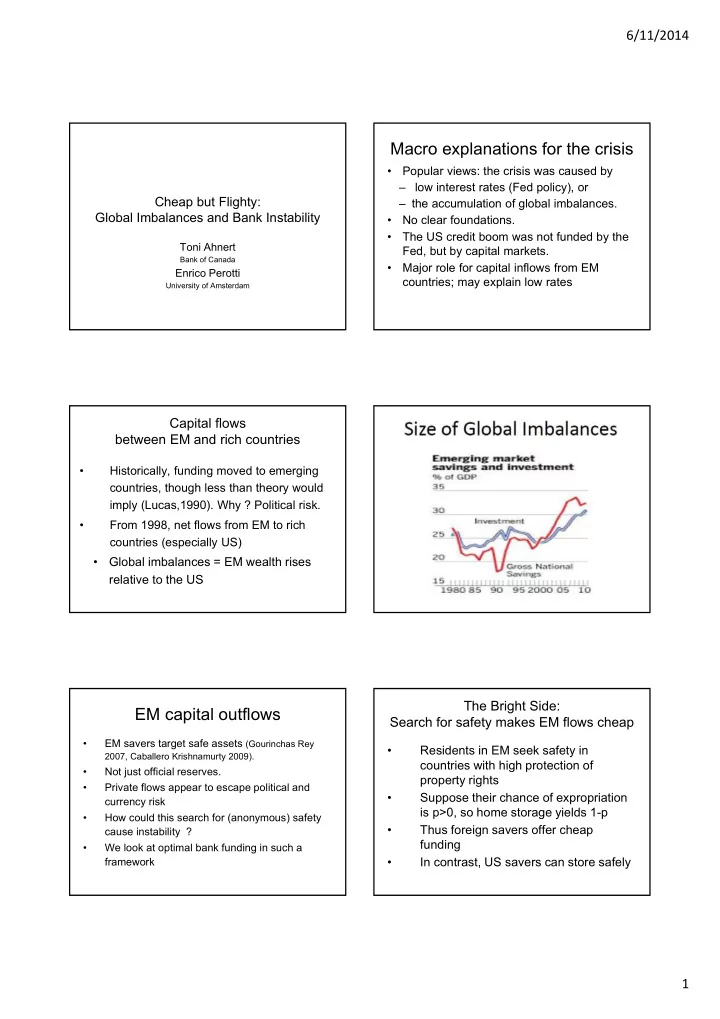

Capital flows between EM and rich countries

- Historically, funding moved to emerging

countries, though less than theory would imply (Lucas,1990). Why ? Political risk.

- From 1998, net flows from EM to rich

countries (especially US)

- Global imbalances = EM wealth rises

relative to the US

EM capital outflows

- EM savers target safe assets (Gourinchas Rey

2007, Caballero Krishnamurty 2009).

- Not just official reserves.

- Private flows appear to escape political and

currency risk

- How could this search for (anonymous) safety

cause instability ?

- We look at optimal bank funding in such a

framework

The Bright Side: Search for safety makes EM flows cheap

- Residents in EM seek safety in

countries with high protection of property rights

- Suppose their chance of expropriation

is p>0, so home storage yields 1-p

- Thus foreign savers offer cheap

funding

- In contrast, US savers can store safely