SLIDE 1

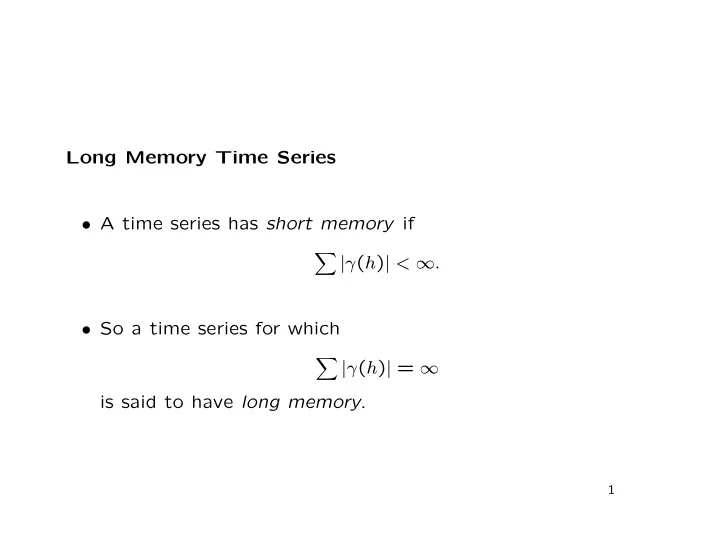

Long Memory Time Series

- A time series has short memory if

- |γ(h)| < ∞.

- So a time series for which

- |γ(h)| = ∞

Long Memory Time Series A time series has short memory if | ( h ) - - PowerPoint PPT Presentation

Long Memory Time Series A time series has short memory if | ( h ) | < . So a time series for which | ( h ) | = is said to have long memory . 1 Why do we care? Write the mean of x 1 , x 2 , . . . , x n as x n