SLIDE 1

IRES

Irish Residential Properties REIT plc – Preliminary Announcement – 31 December 2017

- 1 -

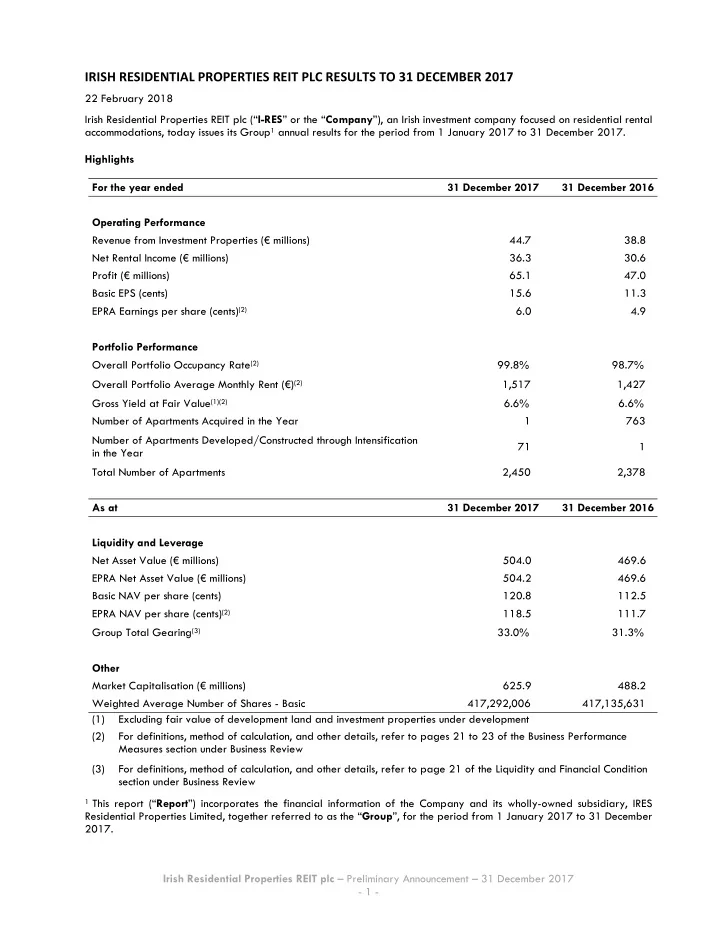

IRISH RESIDENTIAL PROPERTIES REIT PLC RESULTS TO 31 DECEMBER 2017

Review

22 February 2018 23 March 2018 Irish Residential Properties REIT plc (“I-RES” or the “Company”), an Irish investment company focused on residential rental accommodations, today issues its Group1 annual results for the period from 1 January 2017 to 31 December 2017. Highlights For the year ended 31 December 2017 31 December 2016 Operating Performance Revenue from Investment Properties (€ millions) 44.7 38.8 Net Rental Income (€ millions) 36.3 30.6 Profit (€ millions) 65.1 47.0 Basic EPS (cents) 15.6 11.3 EPRA Earnings per share (cents)(2) 6.0 4.9 Portfolio Performance Overall Portfolio Occupancy Rate(2) 99.8% 98.7% Overall Portfolio Average Monthly Rent (€)(2) 1,517 1,427 Gross Yield at Fair Value(1)(2) 6.6% 6.6% Number of Apartments Acquired in the Year 1 763 Number of Apartments Developed/Constructed through Intensification in the Year 71 1 Total Number of Apartments 2,450 2,378 As at 31 December 2017 31 December 2016 Liquidity and Leverage Net Asset Value (€ millions) 504.0 469.6 EPRA Net Asset Value (€ millions) 504.2 469.6 Basic NAV per share (cents) 120.8 112.5 EPRA NAV per share (cents)(2) 118.5 111.7 Group Total Gearing(3) 33.0% 31.3% Other Market Capitalisation (€ millions) 625.9 488.2 Weighted Average Number of Shares - Basic 417,292,006 417,135,631 (1) Excluding fair value of development land and investment properties under development (2) For definitions, method of calculation, and other details, refer to pages 21 to 23 of the Business Performance Measures section under Business Review (3) For definitions, method of calculation, and other details, refer to page 21 of the Liquidity and Financial Condition section under Business Review

1 This report (“Report”) incorporates the financial information of the Company and its wholly-owned subsidiary, IRES