SLIDE 1

Bijzonder actualiteitscollege Leergang Pensioenrecht 28 juni 2011

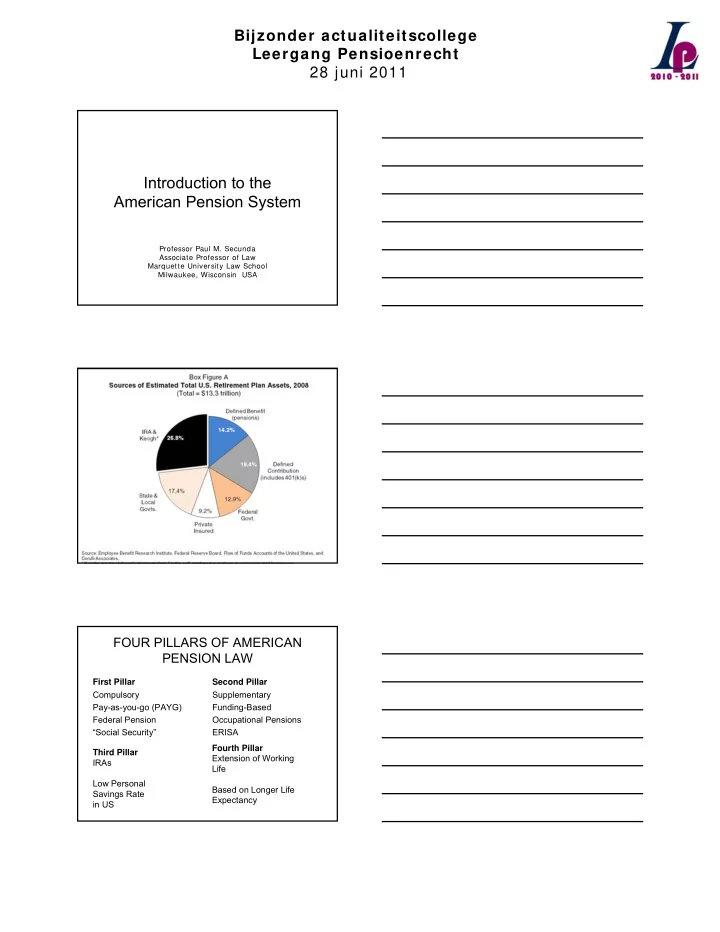

Introduction to the American Pension System

Professor Paul M. Secunda Associate Professor of Law Marquette University Law School Milwaukee, Wisconsin USA

Chapter Three

Introduction to the American Pension System Professor Paul M. - - PDF document

Bijzonder actualiteitscollege Leergang Pensioenrecht 28 juni 2011 Introduction to the American Pension System Professor Paul M. Secunda Associate Professor of Law Marquette University Law School Milwaukee, Wisconsin USA Chapter Three FOUR

Professor Paul M. Secunda Associate Professor of Law Marquette University Law School Milwaukee, Wisconsin USA

Chapter Three

Social Security alone does not provide adequate retirement For large majority of US workers, Social Security will lead to about 40% income replacement ratio (SSA 2011). Yet, to maintain a comfortable lifestyle in post-retirement years, a US worker will need at least 70% to 80% income replacement ratio

As proportion of retirement income replaced by Social Security decreases, proportion replaced by

Consequently, many higher-salaried US employees must receive much larger percentage of retirement from

adequate retirement Or, of course, additional personal savings (third pillar)

June 28, 2011

continuing income after retirement

June 28, 2011

makes while working

issue; intergenerational transfers)

Security benefits

when they were born. If they were born in 1929 or later, workers need 40 credits (10 years of work)

June 28, 2011

Social Security), benefit will be lower than if you wait until later to retire

1960 or later

do, can increase future Social Security benefits in two ways

– Each additional year of work adds another year of earnings to Social Security

– Also, benefit will increase automatically by a certain percentage from the time

June 28, 2011

employees of non-profits

because their states and the Social Security Administration entered into special agreements called “Section 218 agreements”

July 1991 when Social Security was extended to state and local employees who were not covered by an agreement and were not members of their agency’s public pension system.

income up to $106,800 for 2010 at a rate of 6.2% for both the employee and employer

$1,177 at the beginning of 2011or $14,124 per year. The poverty line for

for a worker retiring at age 66 in 2011, the amount is $2,366 per

every year after age 21

lower than if had worked steadily.

June 28, 2011

average wages since the year the earnings were received

during the 35 years in which the worker earned the most

"primary insurance amount" (PIA), is determined

retirement age—65 or older, depending on date of birth

June 28, 2011 June 28, 2011

June 28, 2011

June 28, 2011

DEFINED BENEFIT PLANS DEFINED CONTRIBUTION PLANS Benefits determined by set formula (e.g., 2 percent times years of service times final average pay) Benefits determined by contributions and investment earnings (e.g., 10 percent of annual pay) Funding flexibility Possible discretion in funding Reward older and longer service employees (backloaded) Significant accruals at younger ages Employees face financial penalties for working past normal retirement age No disincentives for working past normal retirement age Long vesting period (e.g., 5 years) Often a short vesting period (e.g., 1 year) Employer bears the investment risk Employee bears the investment risk Employee has no investment discretion Employee has investment discretion High rates of return Significantly lower average rates of return Often not portable Portable Require actuarial valuation Does not require actuarial valuation Relatively low employee understanding and appreciation Relatively high employee understanding and appreciation Unfunded liability exposure No unfunded liability exposure Provide benefits targeted to income replacement level Does not provide benefits targeted to income replacement level Usual form of benefit payment is monthly income (annuity) Usual form of benefit payment is lump sum distribution Employees cannot borrow Employees may be able to borrow

June 28, 2011

– IRAs hold 27% of all retirement income in United States – IRAs classified into four types (EBRI):

– Average and median IRA individual balance (all accounts from the same person combined) was $69,498 and $20,046 at end of 2008. – 11.1 million unique individuals with total assets of $732.9 billion as of year-end 2008.

2008) (source: Bureau of Economic Analysis, U.S. Department of Commerce)