SLIDE 1

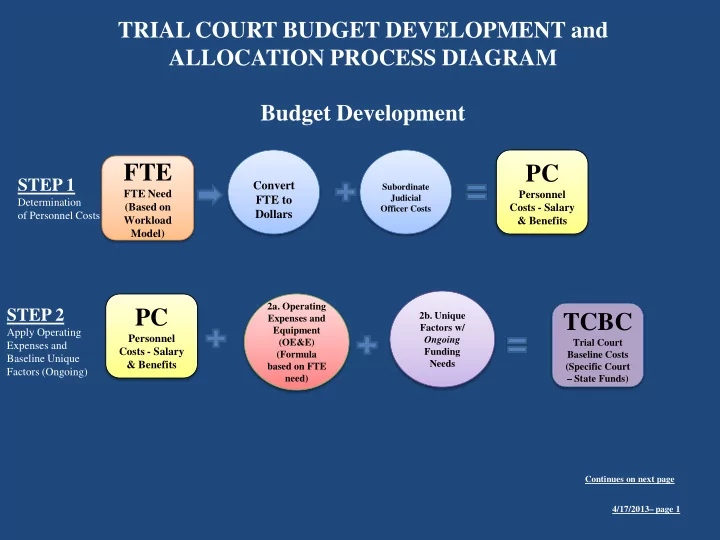

PC

Personnel Costs - Salary & Benefits

STEP 1

Determination

- f Personnel Costs

Convert FTE to Dollars

STEP 2

Apply Operating Expenses and Baseline Unique Factors (Ongoing)

TCBC

Trial Court Baseline Costs (Specific Court – State Funds)

TRIAL COURT BUDGET DEVELOPMENT and ALLOCATION PROCESS DIAGRAM Budget Development

Continues on next page

PC

Personnel Costs - Salary & Benefits

- 2a. Operating

Expenses and Equipment (OE&E) (Formula based on FTE need)

- 2b. Unique

Factors w/ Ongoing Funding Needs

FTE

FTE Need (Based on Workload Model)

Subordinate Judicial Officer Costs 4/17/2013– page 1