SLIDE 1

ST 810-006 Statistics and Financial Risk

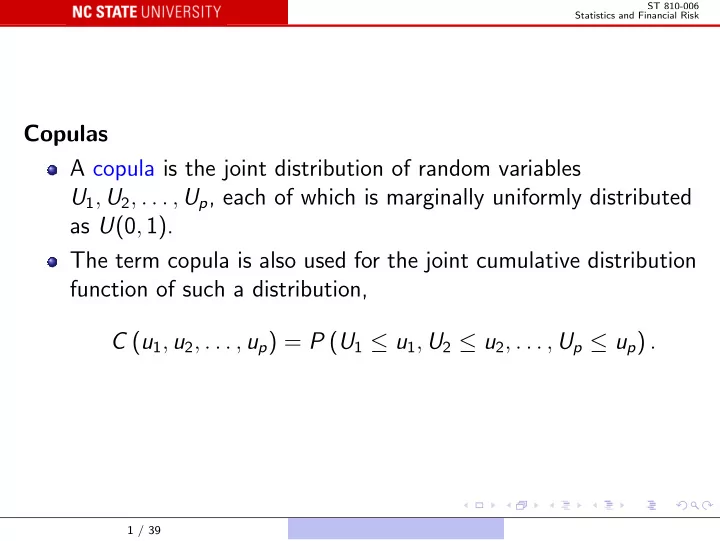

Copulas A copula is the joint distribution of random variables U 1 , - - PowerPoint PPT Presentation

ST 810-006 Statistics and Financial Risk Copulas A copula is the joint distribution of random variables U 1 , U 2 , . . . , U p , each of which is marginally uniformly distributed as U (0 , 1). The term copula is also used for the joint

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

0.5 0.5 1 1 1.5 1.5 2 2 2.5 2.5 3 4

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

1 1 2 2 3 3 5 5

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

0.8 0.8 0.8 0.8 1 1 1 1 1.2 1.2 1 . 2 1.2

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk

ST 810-006 Statistics and Financial Risk