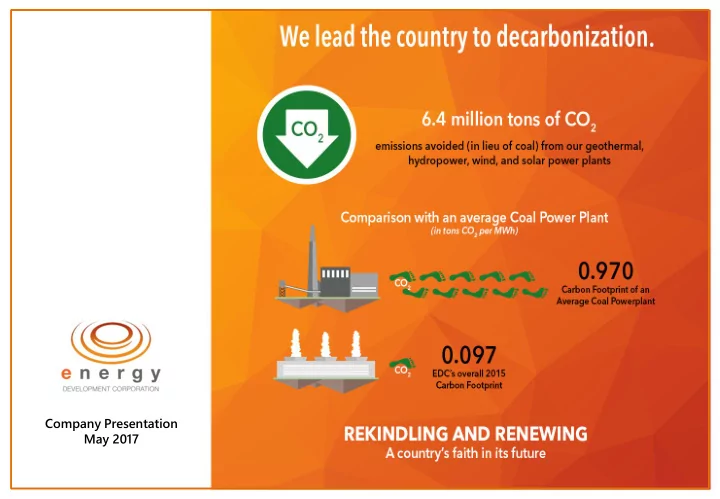

SLIDE 1

Company Presentation May 2017

Company Presentation May 2017 DISCLAIMER This presentation contains - - PowerPoint PPT Presentation

Company Presentation May 2017 DISCLAIMER This presentation contains certain forward looking statements. These forward looking statements include words or phrases such as EDC or its management believes, expects,

Company Presentation May 2017

This presentation contains certain “forward looking statements.” These forward looking statements include words or phrases such as EDC or its management “believes”, “expects”, “anticipates”, “intends”, “plans”, “foresees”, or other words or phrases of similar import. Similarly, statements that describe EDC’s objectives, plans or goals also are forward-looking statements. All such forward looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. Such forward looking statements are made based on management’s current expectations or beliefs as well as assumptions made by, and information currently available to,

information contained herein and shall not accept any responsibility or liability (including any third party liability) for any loss or damage, whether or not arising from any error or omission in compiling such information or as a result of any party’s reliance or use of such information. The information and opinions in this presentation are subject to change without notice. This presentation does not constitute a prospectus or other offering memorandum in whole or in part. Information contained in this presentation is a summary only and is prepared for discussion purposes and is not a complete record of the discussions. This presentation shall not constitute an offer to sell or the solicitation of an offer to buy any security. There shall be no sale of these securities in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to qualification under securities laws of such state or jurisdiction. By receiving this presentation, each investor is deemed to represent that it is a sophisticated investor and possesses sufficient investment expertise to understand the risks involved. Prospective investors should undertake their own assessment with regard to their investment and they should obtain independent advice on any such investment’s suitability, inherent risks and merits and any tax, legal and accounting implications which it may have for them.

In the context of a challenging competitive environment, we are focused in reducing our spot market exposure, investing to improve our equipment’s reliability and resiliency, and in managing our FX exposure EDC currently focusing on solar. Company also see breaking into the contestable markets as key to further reducing WESM exposure

8 Brief Overview - FPH, 9 Summary of Operating Assets, 10 Business Model, 11 Contract Tenor, 12 Portfolio Expansion, 13 Risk Factors & Initiatives

Com

Introductio ion

28 Solar business expansion, 29 Contestable Customers

Bre reaking into New Mark rkets

Key Takeaways

Add ddressin ing Risk Fa Factors rs

16 Reduce Spot Market Exposure, 19 Improve Equipment Reliability and Resiliency, 23 Manage Debt and FX Exposure

EDC is part of the Lopez group of companies … the world’s largest vertically-integrated geothermal company, delivering clean and renewable energy EDC to continue with initiatives to promote earnings predictability, to explore new prospects opportunistically, and to keep its dividend policy.

8 Company Introduction

USD2.13B

FPH’s consolidated revenues for 2015

USD0.26B

FPH’s consolidated net income for 2015

USD7.19B

Total assets in 2015

POWER GENERATION PROPERTY MANUFACTURING CONSTRUCTION & ENERGY SERVICES

EDC IS PART OF THE LOPEZ GROUP’S FIRST PHILIPPINE HOLDINGS (FPH) –A DIVERSIFIED HOLDING COMPANY WITH PRINCIPAL INTERESTS IN ENERGY, REAL ESTATE, AND MANUFACTURING

Leading power producer with distinct assets that utilize indigenous, clean and/or renewable fuels supplying 17% of Philippine requirements. Leading residential, commercial, and office building developer as well as the largest contiguous industrial park in the Philippines. Pioneer and leader in electrical manufacturing in the Philippines One of the leaders in power and energy facilities construction

9 Company Introduction

TODAY EDC IS A DIVERSIFIED RENEWABLE ENERGY COMPANY

150.0 MW Burgos 7.85 MW Solar 120.0 MW Pantabangan 12.0 MW Masiway 120.0 MW Bacman I 20.0 MW Bacman II 112.5 MW Tongonan 112.5 MW Palinpinon I 60.0 MW Palinpinon II* 125.0 MW Upper Mahiao 232.5 MW Malitbog 180.0 MW Mahanagdong 50.9 MW Optimization 49.4 MW Nasulo 52.0 MW Mindanao I 54.0 MW Mindanao II

Note: *20 MW Nasuji Power Plant placed on preservation

1 1 1 2 3 1 3 2

Wind Hydro Solar Geothermal (EDC Subsidiary) Geothermal (Integrated)

1

1 1 1 2 3 3 2 1 1

EDC IS THE LARGEST VERTICALLY INTEGRATED GEOTHERMAL COMPANY GLOBALLY

COMPANY

CAPACITY (in MW) STEAM PLANT

1 EDC

1,169 1,169

2 Comision Federal de Electricidad 958 958 3 Enel Green Power 915 915 4 Chevron ~800* ~400 * 5 Ormat 689 749

Source: Bertani, Ruggero, 2010: Geothermal Power Generation in the World 2005-2010 Update Report Note: * net attributable MW

TOP 5 GEOTHERMAL COMPANIES

10 Company Introduction

EDC’S BUSINESS MODEL POSSESSES STABLE AND PREDICTABLE CASH FLOWS

Transco Electric Cooperatives/ Third party customers/ NGCP/ WESM

Subsidiaries

National Power Corporation

Power Supply Agreements (PSAs) Ancillary Services Provider Agreement (ASPA)

Power Purchase Agreements

Steam Sales Agreements (SSA)

Bac-Man Geothermal

Geothermal Resources Sales Contracts (GRSC)

Green Core Geothermal FG Hydro

Electricity Cashflow Electricity Cashflow

Electricity & Ancillary Svcs.

Cashflow Steam

Cashflow or Dividends

Steam

Cashflow or Dividends

Dividends

Burgos Wind

Electricity Cashflow Dividends

Power Supply Agreements

Power Purchase Agreements (PPAs)

Electricity Cashflow

Solar

Electricity Cashflow

Geothermal

% of Consolidated Revenues (1) USD Linkage

Electricity 37% 73%

Sovereign off-take

Electricity 50% 0%

Commercial off-take

Electricity 13% 60%

Feed-in-Tariff

(1) As of Mar. 31, 2017

Customers

Cashflow Energy Flow

11 Company Introduction

EDC’S EXPOSURE TO THE SPOT MARKET PRICES IS ONLY 9%

WESM, 858 NGCP, 237 DU, 1,327 NPC, 3,589 DU, 1,191 Transco, 1,249 DU, 1,161 SPOT 9% 1-2 YRS 11% 3-5 YRS 5% 6-10 YRS 46% 11-20 YRS 17% >21 YRS 12%

9,612

(1) Consolidated revenues as of March 31, 2017

TERM STRUCTURE OF CONTRACTS(1) In PHP Millions

SPOT 1-2 YRS 3-5 YRS 6-10 YRS 11-20 YRS >21 YRS WESM

9%

5% 9% 4% 12%

NPC

revenue from long-term contracts

revenue from contract tenors

expanded revenue base from contracted commercial clients

12 Company Introduction

HOWEVER, REPORTED EARNINGS HAVE BEEN VOLATILE

19,007 20,527 20,678 24,153 24,540 28,369 25,656 30,867 34,360 34,236 10,324 11,859 10,712 13,748 13,238 17,330 15,641 17,922 18,680 20,736 6,243 5,690 7,276 6,638 4,459 8,522 6,568 9,197 8,798 9,155

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

RE REVENUES EB EBITDA RN RNIA

638 770 1,181 1,331 1,262 1,262 1,262 1,446 1,455 1,458

513 132 411 150 (69) 184 9 2.66

+ 49.4 MW N.Negros + 463.4 MW Mahanagdong, Malitbog & Optimization + 132.0 MW Pantabangan- Masiway + 106.0MW Mindanao I & II + 305.0 MW Palinpinon & Tongonan + 150 MW BacMan I & II

Botong

+ 49.4 MW Nasulo

+ 150.0 MW Burgos + 5.0 MW Bacman Unit 1 + 5.0 MW Bacman Unit 2 + 4.16 MW Burgos Solar + 2.66 MW Burgos Solar Cumulative MW Current MW

Customer Base

3.7 Bn DUs 3.6 Bn NPC 0.9 Bn WESM 1.2 Bn TransCo 0.2 Bn NGCP

Technology

1,169 MW Geothermal 150 MW Wind 132 MW Hydro 7.85 MW Solar

Geography

EDC TODAY

(AS AS OF OF 1Q Q 2017) 7)

2007-2016 (CAGR)

MWcum 9.6% Revenues 6.8% EBITDA 8.1% RNIA 4.4%

13 Company Introduction

WE HAVE CLEAR ACTION PLANS TO REDUCE/ELIMINATE VOLATILITY

Power plants: “Midlife” stage br brings abou bout t reliability iss ssue ues Ma Market: t: Ma Margin sq sque ueeze due due to

com commodity ty pr prices Ge Geography: Project t si sites are si situ tuated along the “typhoon” belt Ge Geoth thermal Re Reso sour urce: Na Natu tural dec decline of

servoir pr pressure Ge Geoth thermal Gr Grow

th CAPEX: : Si Significant amou mounts ts requ quired upfr upfron

FCRS: : Moun Mounta taino nous locat

expos

nfrastructu ture to

potenti tial landslide risk sk Re Retro trofit agi ging g pl plants ts to

nhance ove

reliability ty Re Re-negoti tiate exp xpiring ng cont contracts to

preserve revenu nue ba base Typ yphoon n pr proo

f cr critical powe power pl plant t com components Ad Advanced techn hnologies drive company’s replacement well dr drilling st strategy Ex Expand to

chnolog

and nd acc ccess mul multi ti-late teral fina nancing to

miti tigate te exp xploration

sk In Insti stitute te a proa

ndslide mi miti tigation st strategy

RISK FACTORS INITIATIVES

Power plant lant reh rehab CAP CAPEX Mit itig igate mar argin in sq squeeze Ty Typhoon proo roofin ing CA CAPEX/OPEX Main intenance CA CAPEX Do Domest stic ic grow growth Ty Typhoon proo roofin ing CA CAPEX/OPEX

IMPACT

16 Addressing Risk Factors

WEAK COMMODITY PRICES EXPOSE OUR UNCONTRACTED CAPACITY TO LOWER MARGINS WHICH PROMPTED EDC TO FOCUS ON ASSET RELIABILITY PROGRAMS AND SELECTIVELY POSTPONE GROWTH

5.2 .20 6.4 .48 4.9 .98 3.68 2.78

1.00 3.00 5.00 7. 7.00 9.00 11.00 13.00 15.00 17. 7.00 19.00

2012 2013 2014 2015 2016

Monthly Annual Ave.

WESM PRICES

128.08 8 71.34 34 98.97 97 121.55 5 96.53 53 85.12 12 70.88 88 59.38 38 66.42 42 49.27 27 52.15 15 52.42 42 50.73 73 51.27 27 53.40 40 61.71 71 67.38 38 72.06 06 90.82 82 105.96 6 89.92 92 92.50 50 83.00 00 40 60 60 80 80 100 120 140

2008 2009 2010 10 2011 11 2012 12 2013 13 2014 14 2015 15 2016 16 Jan Jan-16 16 Feb-16 16 Ma Mar-16 16 Apr pr-16 16 Ma May-16 16 Jun-16 16 Jul-16 16 Aug-16 16 Sept-16 16 Oc Oct-16 16 Nov

16 Dec Dec-16 16 Jan Jan-17 17 Feb-17 17

COAL PRICES

Php/kWh $/MT

17 Addressing Risk Factors

TOTAL CONTRACTED CAPACITY OF BOTH BGI AND NASULO IS EXPECTED TO INCREASE FROM 65% IN DECEMBER 2016 TO 92% IN DECEMBER 2017, MINIMIZING LOW SPOT MARKET PRICE RISKS.

92 92 114 114 122 41 41 19 19 11 11

50 70 90 110 130 150

December 2016 May 2017 December 2017

26 26 22 22 22 22 20 20 21 21 24 24 4

10 20 30 40 50

December 2016 May 2017 December 2017

BACMAN NASULO

133 MW

Net Capacity

47 MW

Net Capacity

CONTRACTED CAPACITY ASPA UNCONTRACTED CAPACITY

92% 92% 76% 65% 65%

Dec. 2017 May 2017 Dec. 2016

8% 8% 24% 4% 35% 35%

CONTRACTED VS. WESM (Bacman & Nasulo)

Uncontracted / WESM Exposure Contracted

18 Addressing Risk Factors

FG HYDRO IS EXPECTED TO BE FULLY CONTRACTED BY DECEMBER 2017 BY SELLING 60MW OF ITS CAPACITY TO ASPA. MARKETING IS AGGRESSIVELY SOLICITING ACCOUNTS IN THE PIPELINE.

FG HYDRO

125 MW

Net Capacity

35 35 36 36 36 36 60 91 91 90 90 30 30

20 40 60 80 100 120 140 December 2016 May 2017 December 2017 Contracted Capacity ASPA Uncontracted Capacity Potential DU/EC Account

120MW PANTABANGAN HYDRO PLANT 12MW MASIWAY HYDRO PLANT

19 Addressing Risk Factors

2017 UNPLANNED OUTAGE FACTORS OF MAIN PLANTS HAVE IMPROVED SIGNIFICANTLY WITH IMPLEMENTATION OF RETROFIT / REHAB STRATEGY

END ND OF OF DE DESI SIGN LIFE (HI HIGH) H) END ND OF OF DE DESI SIGN LIFE (LOW) OW) END ND OF OF DE DESI SIGN LIFE (BASE ASELINE)

< < 5% 5% UOF

UNPLANNED OUTAGE FACTOR (UOF)

As of YTD March 2017 Malitbog

0.04%

Palinpinon I

0.77%

Palinpinon II

1.76%

Bacman I

2.58%

Mahanagdong

1.74%

Mindanao II

0.00%

Nasulo

0.15%

Tongonan Units 2 & 3

0.04%

Bacman II

0.22%

Mahanagdong B 2.71%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

5 10 15 20 25 30 35

Upper Mahiao

14.9 .92%

Tongonan Unit 1

40.3 .30%

Mindanao I

9.87%

Leyte Optimization Plants

45.9 .96%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 5.0%

≥ 5% UOF

retrofitted Feb 2017 1 of 4 STG rotors retrofitted for retrofit June-Oct 2017 rehab 2012; CSI 2018 CSI 2016 retrofit 2014 relocated 2014 rehab 2013

PLANT AGE, in years

Leyte Southern Negros Bacman Mindanao

20 Addressing Risk Factors

EDC REMAINS COMMITTED TO BRING UNPLANNED OUTAGE FACTOR (UOF) TO BELOW 5% BY ADDRESSING FLEET WIDE LIFE CYCLE RELIABILITY ISSUES

RELIABILITY IMPROVEMENT STRATEGIES:

21.88% 7.45% 41.34%

125 MW Upper Mahiao 112.5 MW Tongonan 50 MW Leyte Optimization Plants

14.92% 40.30% 45.96%

Unpla lanned Outa tage Fac Factor (UOF)

FY FY 2016 016 YT YTD Mar ar. . 2017 017 Unit 1 – retrofitting and Control System Integration (CSI) works completed, returned to service in Feb 2017 Unit 2 – outage commenced April 19, 2017. Target completion is June 22, 2017. Unit 3 – re-scheduled for June 27 – August 31, 2017

112.5MW TONGONAN 125MW UPPER MAHIAO

Unit 3 – completed the installation of 1st new rotor and diaphragm, returned to service on Sept 2016 Unit 1 – 2nd new rotor installed in Mar 2017 Unit 4 – 3rd new rotor on order with expedited delivery on Aug 2017, for installation Oct 2017 Unit 2 – 4th new rotor on order and for installation 1Q 2018

50MW LEYTE OPTIMIZATION

Mahanagdong A Topping Cycle – new turbine rotor discs on

Tongonan Topping Cycle – new turbine rotor discs on order. Existing rotor discs undergoing repair Malitbog Bottoming Cycle – new rotor procured expected to arrive in 2018

Bacman Unit 3 (Cawayan) is operating normally following the warranty inspection completed last Feb 2016. Comparative UOF registered was 12.77% and 2.27% for FY 2015 and FY 2016, respectively.

21 Addressing Risk Factors

PLANT STEAM RATE IMPROVES BY 10.30% AS UNIT 1 IS FULLY RECOMMISSIONED … IT IS PROJECTED TO IMPROVE BY ~20% AS UNIT 2 RETURNS TO SERVICE BY END JUNE

Retrofit/Control System Integration (CSI) Project Timeline

2.00 2.40 2.80 3.20 3.60 4.00 00

1/1 1/8 1/15 15 1/22 1/29 2/5 2/12 12 2/19 19 2/26 3/5 3/12 12 3/19 19 3/26 4/2 4/9 4/16 16 4/23 4/30 5/7

Unit 1 Unit 2 Unit 3 Plant Steam Rate

Tongonan I Plant Steam Rate

3.31 kg/kW s*

UNIT 1 OPERATING (bet. 37.5MW – 41MW)

2.96 kg/kW s*

kg/kW s

Retrofitting Unit 1

2016 2017 Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Unit 1 Unit 2 Unit 3

Legend: Original Schedule Revised Schedule Reliability Run UNIT 2 ON OUTAGE

2.79 kg/kW s*

*Average Plant Steam Rate

22 Addressing Risk Factors

M1 GENERATOR STATOR WAS REPLACED WITH A BRAND NEW UNIT TO ADDRESS HIGH PARTIAL DISCHARGE THAT DETERIORATED THE STATOR COMPONENTS

Old Generator Assembly New Generator Assembly

Installation work of New Stator

OTHER MAJOR ACTIVITIES

Generator Rotor Retaining Ring

which is the common failure among the generator rotor

Steam Turbine Major Outage

Cooling Tower Modification and Upgrade

23 Addressing Risk Factors

LOANS % BY CURRENCY

Eliminated JPY exposure starting 2011

USD EXPOSURE**

Significant portion of USD obligation remain exposed to currency fluctuations Cash flow exposure is evident in year 2021

CASH FLOW EXPOSURE*

12 66 56 63 62 60 62 62 11 21 44 37 38 40 38 38 77 13 0% 20% 40% 60% 80% 100% 2009 2010 2011 2012 2013 2014 2015 2016

PESO USD JPY

Uncovered Portion 178

* 2021 Parent exposure reduced by ~USD 70MN of dollar bond buyback and assumed current cash to be held until dollar bond maturity exclusive of USD50Mn accumulation ** 2017 Consolidated Year-End Projected figures as of March 31, 2017

1 Remaining Debt Service payments for the year 2 Remaining Opex and Capex unspent for the year 3 Cross Currency Swaps

USD Cash 50 Debt Service 112 CCS 63 Opex & Capex 112 Call Spread 46 80MN Club Loan 73 USD-linked Revenues 99 Dollar Bonds 230 Burgos PHP Exposure 89 USD Uncovered 80

100 150 200 250 300 350 400 450 USD Cover USD Debt

82 60 26 27 316 79 54 20 22 244

50 100 150 200 250 300 350 2017 2018 2019 2020 2021

USD Expenses (New) USD Expenses (Old)

99

USD Linked Revenues

Original Amt: $300Mn

VARIOUS INITIATIVES HAVE BEEN UNDERTAKEN TO INSULATE EDC FROM SWINGS IN NET INCOME

24 Addressing Risk Factors

DELIBERATELY MANAGING FINANCIAL RISKS …

69% 69% 71% 71% 67% 68% 68% 69% 69% 70% 70% 71% 71% 72% 72%

20 40 60 80 100 120 2014 2015 2016 2017E Hedged Unhedged US$ Mn

52% 66% 68% 64% 20% 30% 40% 50% 60% 70% 80%

20 40 60 80 2014 2015 2016 2017E* Amortizing Bullet

5.9% 6.3% 6.2% 5.8% 4% 5% 5% 6% 6% 7% 7%

50 55 60 65 70 75 2014 2015 2016 2017E Total Debt

ANNUAL DEBT SERVICE REQUIREMENT INTEREST RATE LOANS BY REPAYMENT SCHEDULE

71% hedged Interest rate (wtd ave.) reduced to 6.1% Amortizing loans smoothen lumpy principal payments PhP Bn PhP Bn E = estimated % assuming no new financing

25 Addressing Risk Factors

... BRINGS ABOUT A ROBUST BALANCE SHEET

Notes: Ratios are computed based on Parent Company financial statements for DSCR (1) Debt Service Coverage Ratio = Net Cash flow from Operating Activities / (Short Term Debt + Long Term Debt + Projected Interest Service for the next 12 months) (2) EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization

COMFORTABLY OPERATING WITHIN COVENANTED FINANCIAL RATIOS

Total Equities Total Liabilities

94.30 135. 35.81 81

Dec-12 Dec-16

Tota

Asset sets

PhP Bn 58.87 87 83.00 00 35.43 43 52.81 81

Dec-12 Dec-16

Tota

ties and nd Eq Equi uiti ties

PhP Bn

1Q 2017 1Q 2016 Dec-15 Dec-14 Dec-13 Dec-12 4.9 5.4 7.4 5.4 2.1 3.2 1Q 2017 1Q 2016 Dec-15 Dec-14 Dec-13 Dec-12 2.6 2.9 3.1 3.1 3.3 3.2 1Q 2017 1Q 2016 Dec-15 Dec-14 Dec-13 Dec-12 1.2 1.6 1.7 1.4 3.9 2.5

CURRENT RATIO NET DEBT TO EBITDA(2) DEBT SERVICE COVERAGE RATIO(1)

3.6 times 1.0 times

High liquidity to meet short-term obligations Well within our targeted 3.6 times Strong ability to produce cash to cover debt payments

1.2 times

26 Addressing Risk Factors

DIVIDEND POLICY IS TO DECLARE 30% OF PRIOR YEAR’S RNI

1,485 1,875 1,863 2,250 3,000 1,875 1,500 1,875 1,875 2,624 2,623 2,175 750 1,500 1,875 2,062 2,248 6,243 5,690 7,276 6,638 4,459 8,522 6,568 9,197 8,798 9,155 30% 65% 33% 31% 45% 58% 36% 58% 42% 55% 30%

20% 30% 40% 50% 60% 70% 80% 90% 100% 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cash Divi vidends on

Shares

Special Regular RNIA Payout Ratio

PHP/share 0.099 0.270 0.125 0.120 0.160 0.140 0.160 0.200 0.210 0.260 0.14 Yield 1.7% 4.4% 3.3% 2.4% 2.7% 2.4% 2.4% 3.6% 3.5% 4.5% 2.3%

Payout Ratio PhP Mn

At or about 30% of previous year’s Recurring Net Income subject to i) Debt service requirements and loan covenants, and ii) Implementation of business plans, operating expenses, budgets, funding for new investments and acquisitions, appropriate reserves and working capital.

DIVIDEND POLICY STATEMENT

28 Breaking into New Markets

EDC COMMISSIONED ITS FIRST SOLAR ROOFTOP PROJECT IN THE PHILIPPINES, AND CURRENTLY LOOKING AT FURTHER EXPANSION

Capacity: 1.03 MW Location: Gaisano Capital Iloilo EDC to provide up to 50% of the mall’s daytime load through clean solar energy.

ROOFTOP PROJECT WITH GAISANO CAPITAL

29 Breaking into New Markets

EDC IS ALSO NOW ACTIVE IN SEVEN (7) MARKETS FOLLOWING THE ENACTMENT OF EPIRA (2001) AND RE-LAW (2009)

ST STRATEGIC FOC OCUS PRE EP EPIRA POST EP EPIRA POST RE RE-LAW

CUSTOMERS Na Nati tional Power Co Corp rporation (NPC NPC)

Distri ribution Ut Utilities/Electr tric Co Coop

Wh Whol

ectri ricity Spot pot Ma Market (WESM)

NG NGCP

Tr Transco

Distri ributed Gene Generation

Co Contestable Cus Custo tomers

BUSINESS MO MODEL Pow

urchase Agr greements/ Power Supp upply Agre reements (PP PPAs/PSAs)

Spot

Mark rket t (WESM)

Anc ncillary Serv ervices Pro rovider Agre reement t (AS ASPA PA)

Fee eed-in in-Tarrif (FiT FiT)

DOE Dep epartment Orde der No No.: .: DC20 C2016-04 04-0004 0004 Providing timeliness for compliance with the full implementation of retail competition and open access in the Philippine Electric Power Industry

April 21, 2016

ER ERC Re Resolution No No. . 10, 0, Se Series of 2016 016 A Resolution adopting the revised rules for contestability

May 26, 2016

ER ERC Re Resolution No No. . 11, 1, Se Series of 2016 016 A Resolution imposing restrictions on the operations of distributed utilities and retail electricity suppliers in the competitive retail electricity market

May 26, 2016

Regulations governing retail competition and

30 Breaking into New Markets

WHERE THE CONTESTABLE CUSTOMERS ARE …

Based on February 2017 List published in www.buyyourelectricity.com.ph

Contracted with RES vs. Still being Served By DU

Definition of Terms…

user that has a choice of a supplier of electricity, as may be determined by the ERC. They are presently the following:

1 MW to greater than 750 KW

1MW and greater

below 1 MW to greater than 750 KW

customers (or retail customers) may themselves contract for the supply of electricity with authorized suppliers, rather than through the franchised distribution utility.

electricity customers and suppliers of electricity may also contract with the transmission company and the distribution company for the “wheeling” or delivery of energy/electricity through the transmission

distribution wires.

OPEN ACCESS IS THUS THE MEANS BY WHICH RETAIL COMPETITION IS ACHIEVED.

Contracted with RES Remains with DU

Total Qualified Co Contestable Cu Customers 1,5 ,554 1 MW 1,115 With Retail Supply Contract 661 Who have not switched (Luzon) 349 Who have not switched (Visayas) 105 750 kW 439 With Retail Supply Contract 81 Who have not switched (Luzon) 323 Who have not switched (Visayas) 35

~1, 1,659 MW MW 74 742 2 Cus ustomers ~2,0 ,063 MW MW 812 Customers rs

32 Key Takeaways

KEY TAKEAWAYS

TURBINE RETROFIT REINFORCED COOLING TOWER

EDC commissioned its first solar rooftop project in the Philippines and continues to seek further opportunities to expand its solar utility space

EDC competes in the new market segments [FiT based, Retail Competition and Open Access (RCOA) and Ancillary Services] created with EPIRA and RE Law’s passage

Bre Breaking into nto New ew Mar arkets

EDC REMAINS COMMITTED TO GROW ITS GEOTHERMAL BUSINESS OVERSEAS AND PAY CASH DIVIDENDS TO ITS SHAREHOLDERS

EDC proactively invests in both typhoon resiliency and equipment reliability uprating initiatives to deter operational upsets, in the process lowering unit costs and delivering on ‘financial predictability’.

EDC commits to contract its WESM exposure and to implement cost management initiatives given that a low margin environment is expected to persist.

EDC deliberately manages financial risks by entering into project financing for new investments, hedging of US Dollar debt, and

refinancing bullet maturities to amortizing type loan

EDC comfortably remains within covenanted debt ratios despite the increase in leverage

Add ddressin ing Risk Risk Fa Fact ctors

SOLAR ROOFTOP

www.energy.com.ph