SLIDE 1

Chapter Objectives To determine how much you can afford to spend on - - PDF document

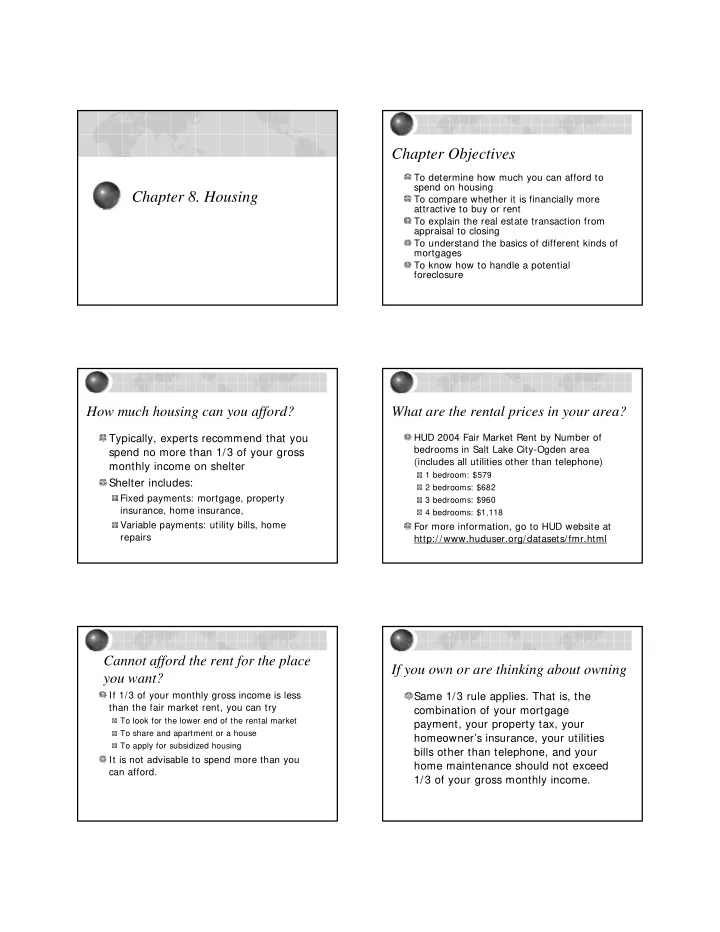

Chapter Objectives To determine how much you can afford to spend on housing Chapter 8. Housing To compare whether it is financially more attractive to buy or rent To explain the real estate transaction from appraisal to closing To understand

Effective Interest Rate on Fixed-Rate Mortgage 1985-2004

0.00 5.00 10.00 15.00 1 9 8 5 1 9 8 7 1 9 8 9 1 9 9 1 1 9 9 3 1 9 9 5 1 9 9 7 1 9 9 9 2 1 2 3 Year Effective rate (%)

$75,600.00

$6,300 Housing Expense Test

28%

$1,764

340

$1,424 expense test

36%

$2,268

$474

$814 debt repayment

$1,454 under debt repayment test

$1,424 (lesser of Line 11 or Line 6) ** Contract rate on home mortgage 8.00% ** Duration of loan (months) 360.00

$7.34

$194,068

0.80

$242,585 Required Down Payment $48,517

Meaning: If a family earns about 85.4% (100/117.1) of median income in the U.S., then this family can qualify for a conventional loan to buy an existing median-priced home. For more information about Housing Affordability Index, go to http://www.realtor.org/Research.nsf/files/REL0506A.pdf/$FI LE/REL0506A.pdf

http://www.huduser.org/datasets/il.html

41%

(lender)