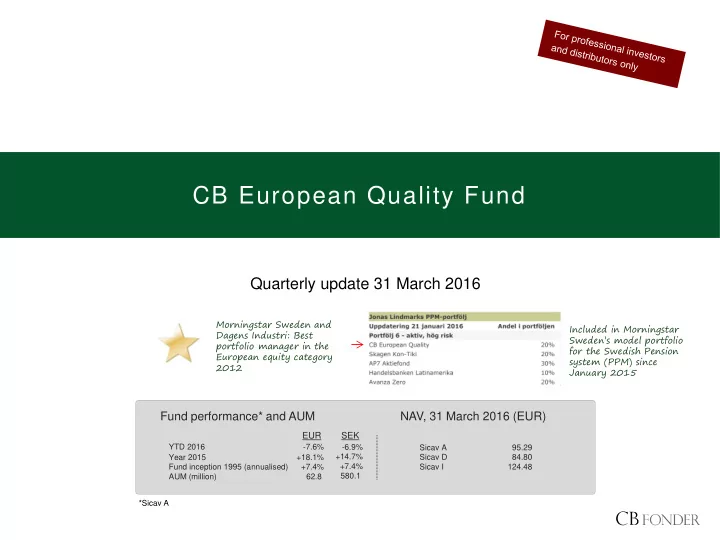

SLIDE 9

- 1,2%

- 1,0%

- 0,8%

- 0,6%

- 0,4%

- 0,2%

0,0% 0,2% 0,4%

The Portfolio: Contributors and detractors

CB European Quality Fund

9

Company Contr./Detr. %

- Avg. weight*, % Performance, %

Top three quarterly contributors and detractors, Q1 2016 (EUR)

*Average values in Q1 2016. Source: Bloomberg, CB Fonder

Kerry Geberit TKH Group Shire Prudential Next Plc +0.30 +0.16 +0.12

+7.3 +5.2 +0.5

4.2 3.9 0.3 3.1 1.2 3.9

- Ireland’s Kerry – a global supplier of additives/ingredients to the food industry – benefit from the increasing outsourcing in terms of manufacturing and

product innovation by the major players (Nestle, Unilever etc.). The company offers its customers complete solutions in taste, texture and nutrition and has delivered an annual profit growth of over 9% per year since 2006. Shares rose 7% during the quarter, in EUR.

- Swiss Geberit is a market leading producer of products for the sanitation and HVAC industries. The company is exposed to a weak business cycle in the

construction sector but have managed to deliver an organic growth of 4-6% annually over the last couple of years through a large market share and exposure to ”the right” markets (Germany and Switzerland). Since their acquisition of Sanitec in 2015 they are also behind well known Nordic brands such as IDO and lfö. The growth is in line with their medium-term objective and the stock rose 5% during the quarter, in EUR.

- TKH Group – a Dutch tech company which delivers telecom, building and industry solutions – was added to the fund in the first quarter. The company is

rather independent of the macro climate; their success builds on more company specific factors (such as increased market share through innovation and acquisition), something they historically have succeeded well with. Their average annual organic revenue growth has been 6% during the period 2006-2015 and their EPS growth has been 14% during the same period. The stock rose 1% during the quarter, in EUR.

- .

- British Shire – market leading in the treatment of ADHD, Gastroenterology and rare genetic disorders – experienced a weak quarter as a result of a weak

stock price development within the biotech and health care sectors. The company has an appealing valuation as a result of the recent decrease in the stock

- price. The stock lost 21% during the quarter, in EUR.

- Prudential – a British insurance company with a focus on Asia, the US and the UK – was hit hard by the general uncertainty regarding the financial stability

in Asia and in China particularly. The stock lost 23% during the quarter, in EUR.

- The British retail company Next – ”the H&M of the UK” – reported in line with expectations regarding the full year 2015 but expressed themselves very

carefully regarding 2016. As a result, the stock lost 31% during the first quarter, in EUR.