SLIDE 19 Analysis: Allocation – Europe versus the U.S.

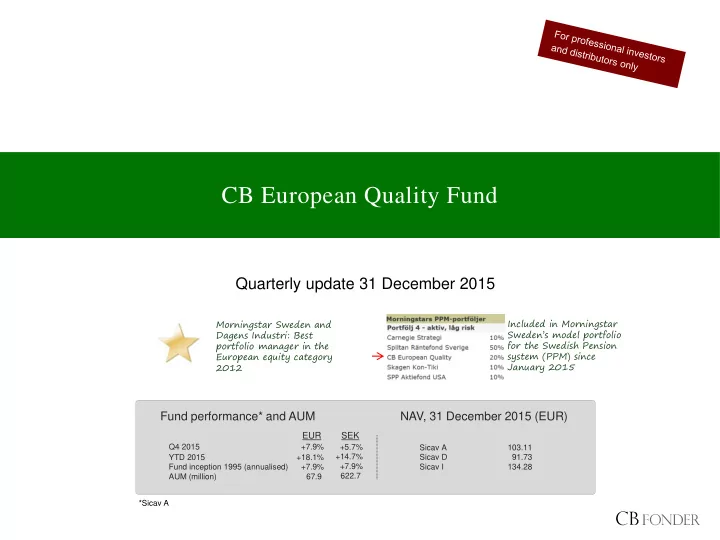

CB European Quality Fund

19

MSCI Europe relative to MSCI USA. Periods of out-/underperformance MSCI Europe relative to MSCI USA, same currency

- Europe has four pronounced periods of

underperformance against the U.S., all

which have bottomed when the accumulated underperformance reached ~40%. This time Europe has underperformed by 43%!

period

stands before Europe? Never before (with data going back to 1969) has Europe underperformed more than current levels. The duration (see table) also speaks for Europe.

From To Duration Months

1 975- 02- 28 1 976- 1 0- 29

8% 30%

20 1 976- 1 0- 29 1 978- 1 0- 31 76%

84% 24 1 978- 1 0- 31 1 985- 02- 28 34% 1 32%

76 1 985- 02- 28 1 990- 1 0- 31 283% 90% 1 02% 68 1 990- 1 0- 31 1 999- 06- 30 224% 451 %

% 1 04 1 999- 06- 30 2007- 1 1

1 02% 1 5% 75% 1 01 2007- 1 1

201 5- 1 2- 31

0% 57%

97

Time period Absolute return (USD) MSCI Europe MSCI USA Relative return

0% 20% 40% 60% 80% 100% 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 MSCI Europe vs MSCI USA Days after first Fed rate hike

EUR/USD after first Fed rate hike (day of hike = 100)

% Months before and after first Fed rate hike MSCI EAFE vs MSCI USA

- Non-US stocks have on average

- utperformed US stocks by 14%

during the 12 months following the first FED rate hike; out of the nine examined periods since 1970, non-US stocks outperformed during six periods (by 22% on average) and US stocks outperformed during three periods (by 4% on average).

- The USD appreciation against the

EUR must subside in

for Europe to outperform the US market; this has been the case in four out of five periods following earlier FED hikes.

Source: MSCI, CB Fonder, Bernstein, Deutsche Bank Research

EUR has performed well relative to USD after prior FED hikes Non-US markets have outperformed the US market following prior FED-hikes

Source: Bernstein, CB Fonder Source: Deutsche Bank Research, CB Fonder