SLIDE 1

CBRE Limited | Page 1

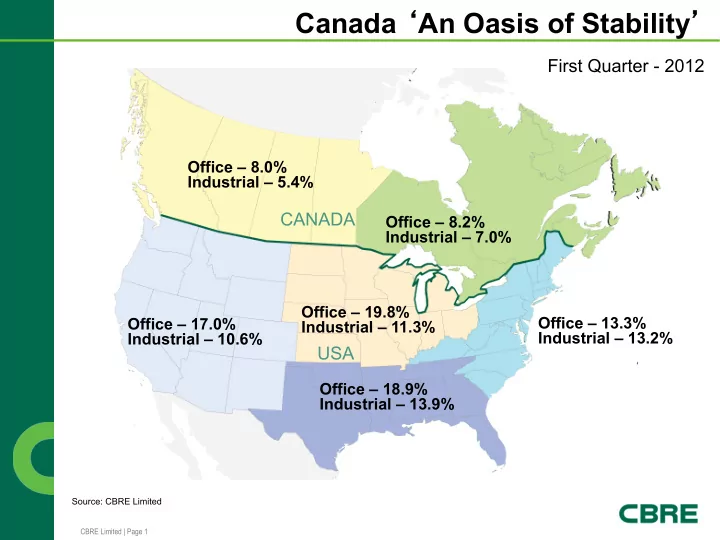

Source: CBRE Limited

Canada An Oasis of Stability First Quarter - 2012 Office 8.0% - - PowerPoint PPT Presentation

Canada An Oasis of Stability First Quarter - 2012 Office 8.0% Industrial 5.4% CANADA Office 8.2% Industrial 7.0% Office 19.8% Office 13.3% Office 17.0% Industrial 11.3% Industrial 13.2%

CBRE Limited | Page 1

Source: CBRE Limited

CBRE Limited | Page 2

Vacancy and Availability Rates

Sources: CBRE-EA 2011Q4 Outlook Report

CBRE Limited | Page 3

CBRE Limited | Page 4

CBRE Limited | Page 5

CBRE Limited | Page 6

CBRE Limited | Page 7

CBRE Limited | Page 8

CBRE Limited | Page 9

Source: CBRE-EA Canada Outlook 4Q 2011

CBRE Limited | Page 10

Source: CBRE Limited

CBRE Limited | Page 11

Source: CBRE Limited

CBRE Limited | Page 12

2016: Bow South

400,000 SF

Matthews Development 2014: 8th Ave. Pl. – west tower

841,000 SF

Hines U/C 2014 Completion 2016: Calgary City Centre

820,000 SF

Cadillac Fairview Permitting/ Preleasing 2016 Completion 2017: Herald Site

1,200,000 SF

Brookfield 2015: Eau Claire Tower

600,000 SF

Oxford Permitting/ Preleasing 2016 Completion Permitting/ Preleasing 2015 Completion Permitting/ Preleasing 2017 Completion

CBRE Limited | Page 13

2015: TELUS Gardens 448,000 SF TELUS/Westbank

Under Construction 2015 Completion

2015-2016: Burrard Gateway 204,000 SF Pattison/Reliance

Permitting/Preleasing

2014: MNP Tower 270,000 SF Oxford Properties

Under Construction 2014 Completion

2015-2016: 980 Howe 270,000 SF Manulife

Permitting/Preleasing

2015: 745 Thurlow Street 365,000 SF Bentall Kennedy

Under Construction 2015 Completion

2015: The Exchange 400,000 SF Credit Suisse/Swissreal

Permitting/Preleasing 2015 Completion

CBRE Limited | Page 14

Source: CBRE Limited/RealNet Canada

CBRE Limited | Page 15

Source: Real Capital Analytics *2011 Unaudited, figures in Billions.

CBRE Limited | Page 16

Sources: Real Capital Analytics, Properties over $2.5 million tracked since 2007. Updated 2.21.12.

*Volume in Millions of $

Market Total Props Total Volume Manhattan 12 $5,632.0 Boston 26 $3,215.0 Los Angeles 16 $2,795.8 San Diego 13 $1,726.1 Houston 40 $1,681.0 Phoenix 80 $1,054.2 DC 7 $969.5 No NJ 11 $884.6 San Jose 8 $829.2 Other 722 $12,001.2 Total 935 $30,788.6

*Volume in millions of $

CBRE Limited | Page 17

Source: CBRE Limited

CBRE Limited | Page 18

Source: CBRE Limited, Bank of Canada

CBRE Limited | Page 19

Source: Bank of Canada

CBRE Limited | Page 20

Source: CBRE Limited, Bank of Canada

CBRE Limited | Page 21

Source: Yahoo! Finance