SLIDE 1

APPLICABILITY OF INTERNAL AUDIT CONT….

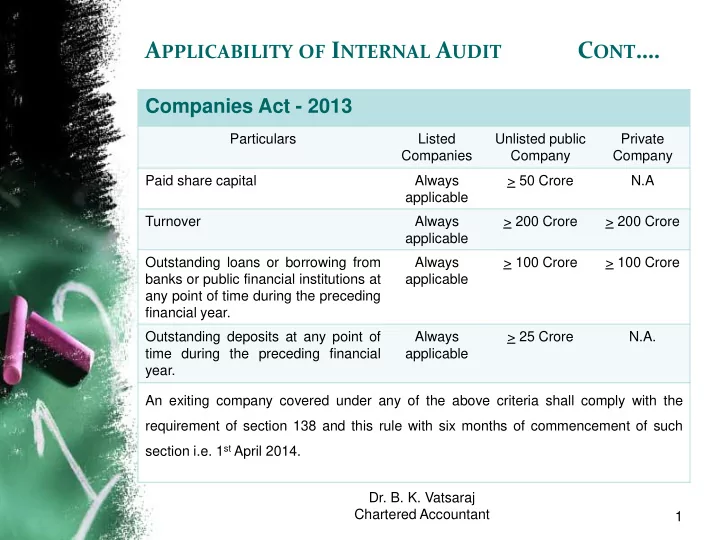

Companies Act - 2013

Particulars Listed Companies Unlisted public Company Private Company Paid share capital Always applicable > 50 Crore N.A Turnover Always applicable > 200 Crore > 200 Crore Outstanding loans or borrowing from banks or public financial institutions at any point of time during the preceding financial year. Always applicable > 100 Crore > 100 Crore Outstanding deposits at any point of time during the preceding financial year. Always applicable > 25 Crore N.A. An exiting company covered under any of the above criteria shall comply with the requirement of section 138 and this rule with six months of commencement of such section i.e. 1st April 2014.

- Dr. B. K. Vatsaraj

Chartered Accountant 1