SLIDE 1

Black-Scholes Price

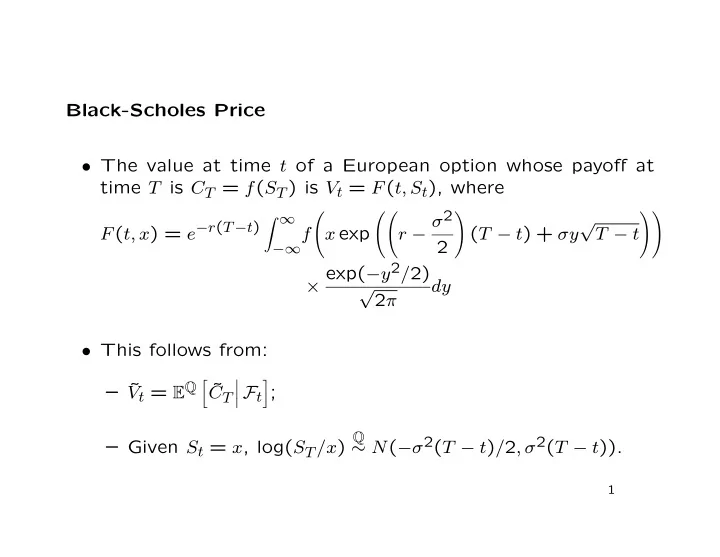

- The value at time t of a European option whose payoff at

time T is CT = f(ST) is Vt = F(t, St), where F(t, x) = e−r(T−t)

∞

−∞f

- x exp

- r − σ2

2

- (T − t) + σy

√ T − t

- × exp(−y2/2)

√ 2π dy

- This follows from:

– ˜ Vt = EQ ˜ CT

- Ft

- ;

– Given St = x, log(ST/x) Q ∼ N(−σ2(T − t)/2, σ2(T − t)).

1