SLIDE 1

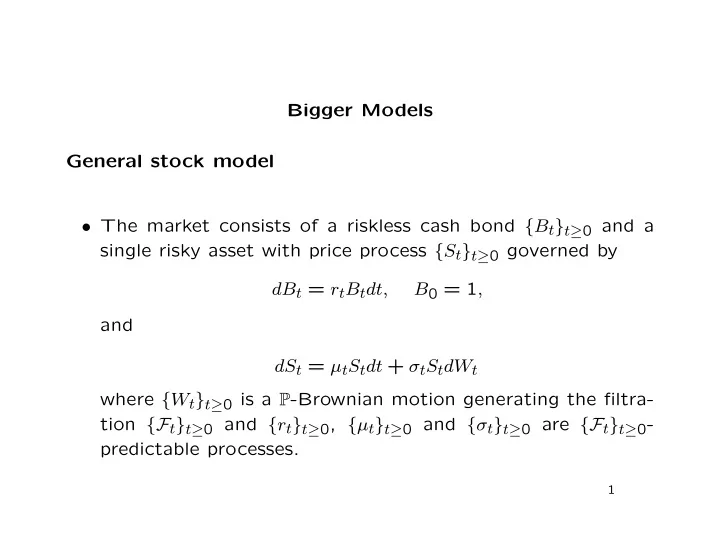

Bigger Models General stock model

- The market consists of a riskless cash bond {Bt}t≥0 and a

Bigger Models General stock model The market consists of a riskless - - PowerPoint PPT Presentation

Bigger Models General stock model The market consists of a riskless cash bond { B t } t 0 and a single risky asset with price process { S t } t 0 governed by dB t = r t B t dt, B 0 = 1 , and dS t = t S t dt + t S t dW t where { W