Enero Group Limited ABN 97 091 524 515 Level 2, 100 Harris Street Pyrmont NSW 2009 Australia

- t. +61 2 8213 3031

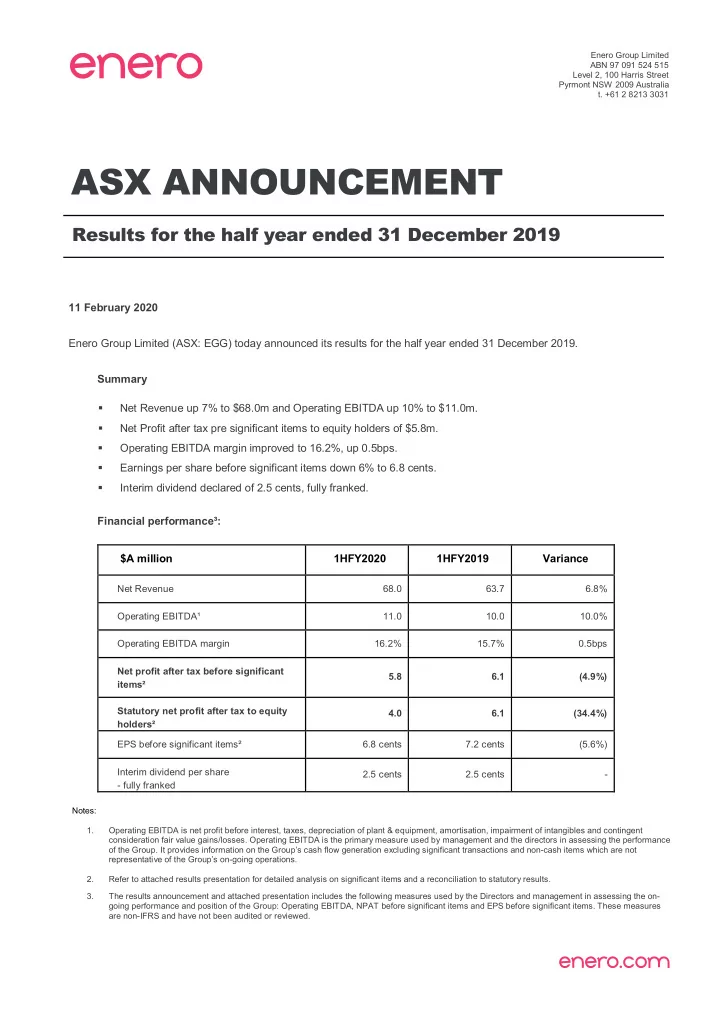

ASX ANNOUNCEMENT

Results for the half year ended 31 December 2019

11 February 2020 Enero Group Limited (ASX: EGG) today announced its results for the half year ended 31 December 2019. Summary

- Net Revenue up 7% to $68.0m and Operating EBITDA up 10% to $11.0m.

- Net Profit after tax pre significant items to equity holders of $5.8m.

- Operating EBITDA margin improved to 16.2%, up 0.5bps.

- Earnings per share before significant items down 6% to 6.8 cents.

- Interim dividend declared of 2.5 cents, fully franked.

Financial performance³: $A million 1HFY2020 1HFY2019 Variance

Net Revenue 68.0 63.7 6.8% Operating EBITDA¹ 11.0 10.0 10.0% Operating EBITDA margin 16.2% 15.7% 0.5bps Net profit after tax before significant items² 5.8 6.1 (4.9%) Statutory net profit after tax to equity holders² 4.0 6.1 (34.4%) EPS before significant items² 6.8 cents 7.2 cents (5.6%) Interim dividend per share

- fully franked

2.5 cents 2.5 cents

- Notes:

1. Operating EBITDA is net profit before interest, taxes, depreciation of plant & equipment, amortisation, impairment of intangibles and contingent consideration fair value gains/losses. Operating EBITDA is the primary measure used by management and the directors in assessing the performance

- f the Group. It provides information on the Group’s cash flow generation excluding significant transactions and non-cash items which are not

representative of the Group’s on-going operations. 2. Refer to attached results presentation for detailed analysis on significant items and a reconciliation to statutory results. 3. The results announcement and attached presentation includes the following measures used by the Directors and management in assessing the on- going performance and position of the Group: Operating EBITDA, NPAT before significant items and EPS before significant items. These measures are non-IFRS and have not been audited or reviewed.