SLIDE 1

Asset Pricing II

April 23, 2004 David has taught you well, but . . .

– Typeset by FoilT EX –

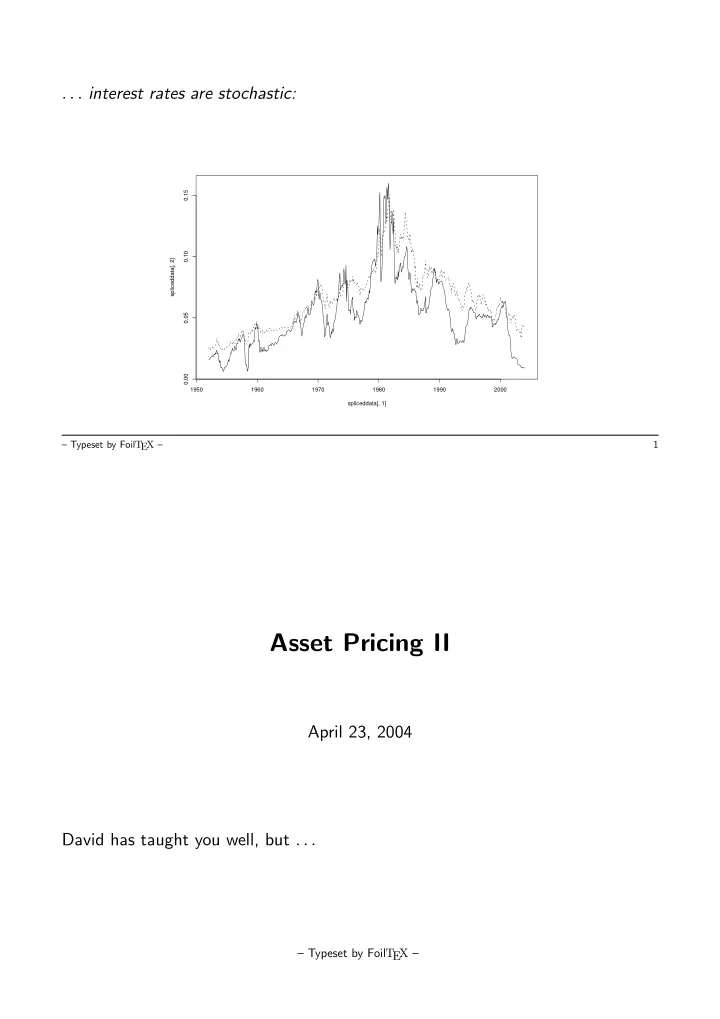

. . . interest rates are stochastic:

1950 1960 1970 1980 1990 2000 0.00 0.05 0.10 0.15 spliceddata[, 1] spliceddata[, 2]

– Typeset by FoilT EX – 1