SLIDE 1

An Introduction to Behavioral Finance

1

Nattawut Jenwittayaroje, Ph.D, CFA NIDA Business School National Institute of Development Administration Master of Arts program in Applied Finance

Topics

- Efficient Market Hypothesis

- Empirical Support of Efficient Market Hypothesis

- Empirical Challenges to the Efficient Market Hypothesis

- Theoretical Challenges of the Efficient Market Hypothesis

- What is Behavioral Finance?

- Applications of Behavioral Finance

- Why Behavioral Finance matters?

2

Efficient Market Hypothesis (EMH)

- Fama (1970): an efficient financial market is one in which

security prices always fully reflect all available information.

- Weak-form: current prices reflect all stock market information (e.g., past

returns and past trading volume).

- Trading rules based on past stock market returns and trading volume are

useless.

- Semi-strong-form: current prices reflect all public information (e.g.,

earnings announcement, P/E and P/BV ratios).

- Trading rules based on public information are useless.

- Strong-form: current prices reflect all public and nonpublic information

- All trading rules are useless.

3 4

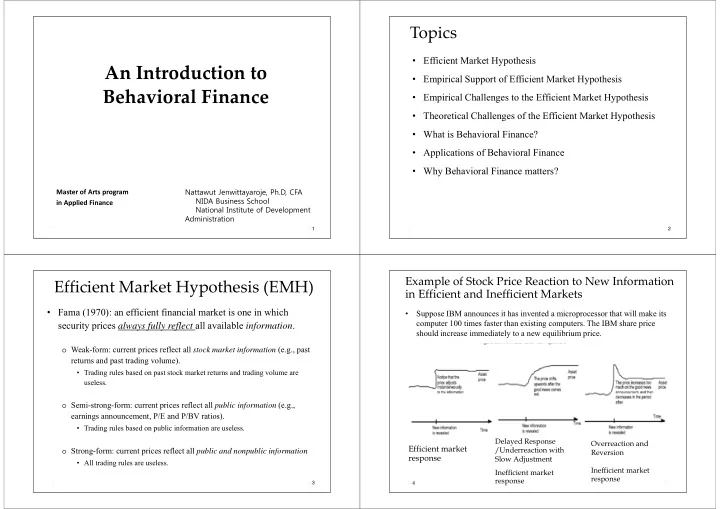

Example of Stock Price Reaction to New Information in Efficient and Inefficient Markets

- Suppose IBM announces it has invented a microprocessor that will make its

computer 100 times faster than existing computers. The IBM share price should increase immediately to a new equilibrium price. Efficient market response

Delayed Response /Underreaction with Slow Adjustment Inefficient market response Overreaction and Reversion Inefficient market response