SLIDE 1

IN CONFIDENCE 4 March 2020 Webinar Slides with speaker notes Good afternoon everyone, and welcome to the webinar. My name is Trish Spence-Manning and I’m an External Relationship Manager at Inland Revenue, working with tax intermediaries and professional bodies from around the country. This is our final webinar for tax agents and bookkeepers for now, and today we’ll go into a bit more detail to help you get ready for when the next set of changes go live in April 2020. Before we start, let’s go over a few housekeeping notes. You’ll see a small control panel at the bottom of your screen and when you click on each of these buttons, you’ll see they either open or close some of the features which may already be open on your screen.

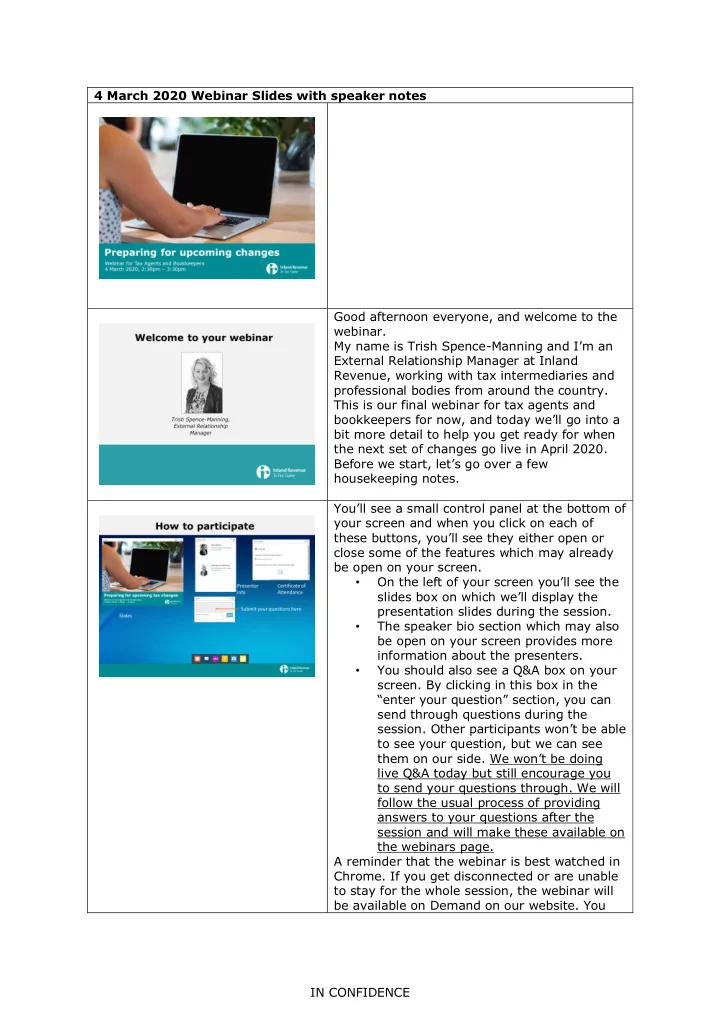

- On the left of your screen you’ll see the

slides box on which we’ll display the presentation slides during the session.

- The speaker bio section which may also

be open on your screen provides more information about the presenters.

- You should also see a Q&A box on your

- screen. By clicking in this box in the

“enter your question” section, you can send through questions during the

- session. Other participants won’t be able

to see your question, but we can see them on our side. We won’t be doing live Q&A today but still encourage you to send your questions through. We will follow the usual process of providing answers to your questions after the session and will make these available on the webinars page. A reminder that the webinar is best watched in

- Chrome. If you get disconnected or are unable