SLIDE 1

The Total Resource Cost Test in Rhode Island Presentation to Rhode - - PowerPoint PPT Presentation

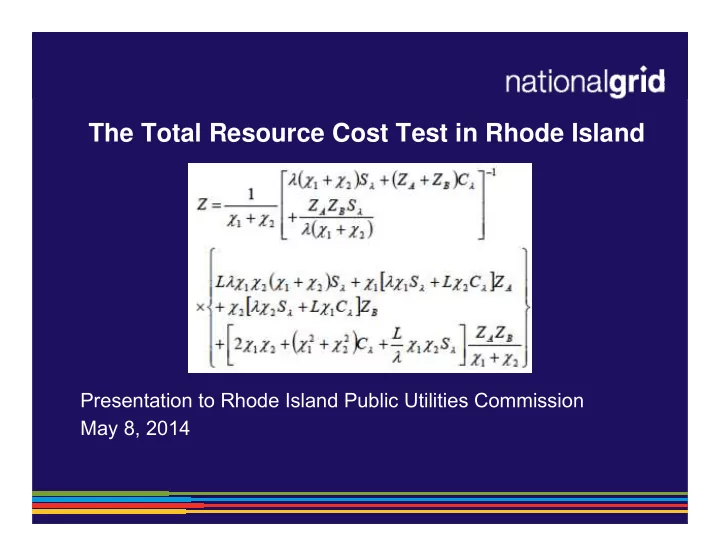

The Total Resource Cost Test in Rhode Island Presentation to Rhode Island Public Utilities Commission May 8, 2014 Agenda PART 1. Current application of the TRC Test in RI Background Why RI uses the TRC Components of TRC

Source: NEEP

6

7

8

9

11

12

13

14

Lifetime Benefits Costs Lifetime Benefits Costs BCR Measure A

$125 $75 125 75 1.67

Measure B

$200 $200 200 200 1.00

Measure C

$150 $100 150 100 1.50

PP&A, marketing, etc.

$50

Total Program

$475 $425 475 425 1.12

15

16

17

18

19

from the energy efficiency measure or program. They are represented by cost factors of $ value per unit savings from regional avoided cost study :

investments from a spreadsheet model developed by an avoided cost study contractor

reductions, low-income service benefits, etc.

20

21

22

23